India Inc’s strong Q2 earnings mask a shallow recovery

An analysis of 3,906 listed companies reporting earnings as of Nov. 19 found that India Inc.’s overall aggregate revenue rose 7.5% year-on-year in the September quarter. This was the strongest revenue pressure in the last four quarters, while net profit increased by 34%, the highest level since the second quarter of FY24.

Meanwhile, operational revenue increased 6.5% year-on-year and 2% sequentially. The annual pressure is the strongest in the last five quarters and is slightly above the nine-quarter average of 6.4%. In other words, India Inc.’s strong performance in the second quarter of FY26 included only a modest increase in sales volumes.

In contrast, other revenues increased by almost 50% year-on-year and 36% compared to the previous quarter. This was the largest non-core revenue pressure in nine quarters and added a disproportionate weight to total revenue and profitability in the second quarter.

However, Nuvama Institutional Equities noted that only the cement, chemicals and automobile sectors achieved meaningful margin expansion, raising the risk that India Inc.’s profit margins may have peaked in the second quarter.

Ajit Mishra, senior vice president of research at Religare Broking, said the first signs of margin pressure were seen in the industrial, consumer and services sectors in the September quarter, indicating profit normalization thereafter.

“Softer inflation, “Rate cuts and policy support could help, but without stronger demand growth, profitability is unlikely to meaningfully outpace revenues,” he added.

India Inc.’s second-quarter profit growth was positive thanks to oil marketing companies (OMCs) rebounding sharply from an abnormally low base, said N. Aruna Giri, CEO of equity research and asset management firm TrustLine Holdings. “Banks, meanwhile, delivered only low single-digit profit growth. Removing both banks and OMCs provides a more accurate read of underlying second-quarter performance,” he added.

volume revival

The analysis showed that without OMCs, banks, financial services and insurance (BFSI) companies, India Inc’s net profit rose 45% year-on-year, reaching its highest level since the second quarter of FY24. The analysis showed that the sharp rise was driven by a near doubling of non-core revenue, marking the strongest increase since a slight 2% decline in the second quarter of FY24.

This was supported by better volume-oriented operating leverage in select sectors, softer input costs reflected in falling wholesale inflation and continued strength in mid- and small-cap companies, according to Manish Jain, head of fund management at Centrum Broking.

“Midmarket companies drove the bulk of revenue and profit growth thanks to superior execution,” he added. “After Covid, companies increased profitability by becoming leaner and more disciplined regarding investment expenses,” he added.

Most importantly, India Inc’s sales volumes (excluding OMCs and BFSI) rose 8% year-on-year, well above the nine-quarter average of 5.7%. Consensus indicators pointed to strong domestic demand for telecoms and automobiles, and the jewelery segment to be unexpectedly resilient despite rising gold prices, helping stabilize volumes. Stronger-than-expected performances in cement and non-ferrous metals further boosted overall volume growth.

Religare Broking’s Mishra added that industrial, capital goods and defense-related companies also delivered positive surprises, supported by strong order books and government capital spending momentum.

But discretionary categories such as hotels, consumer durables, mass-market fashion and quick-service restaurants saw an uneven recovery, according to Antique Stock Broking. Consumer staples remained stable but there were no meaningful volume increases.

Consumer demand remained solid but did not accelerate in the second quarter as households channeled earlier income tax cuts into deleveraging, with only GST cuts boosting consumption meaningfully towards the end of September, Centrum Broking’s Jain said. Kotak Institutional Equities similarly flagged volume softness due to GST-related purchasing deferrals, even as urban demand started to slowly pick up.

shallow recovery

However, Jain said the latest earnings report signaled a selective recovery and a broad-based recovery was still missing. “Even sectors that appear stable are supported by their most powerful players,” he added.

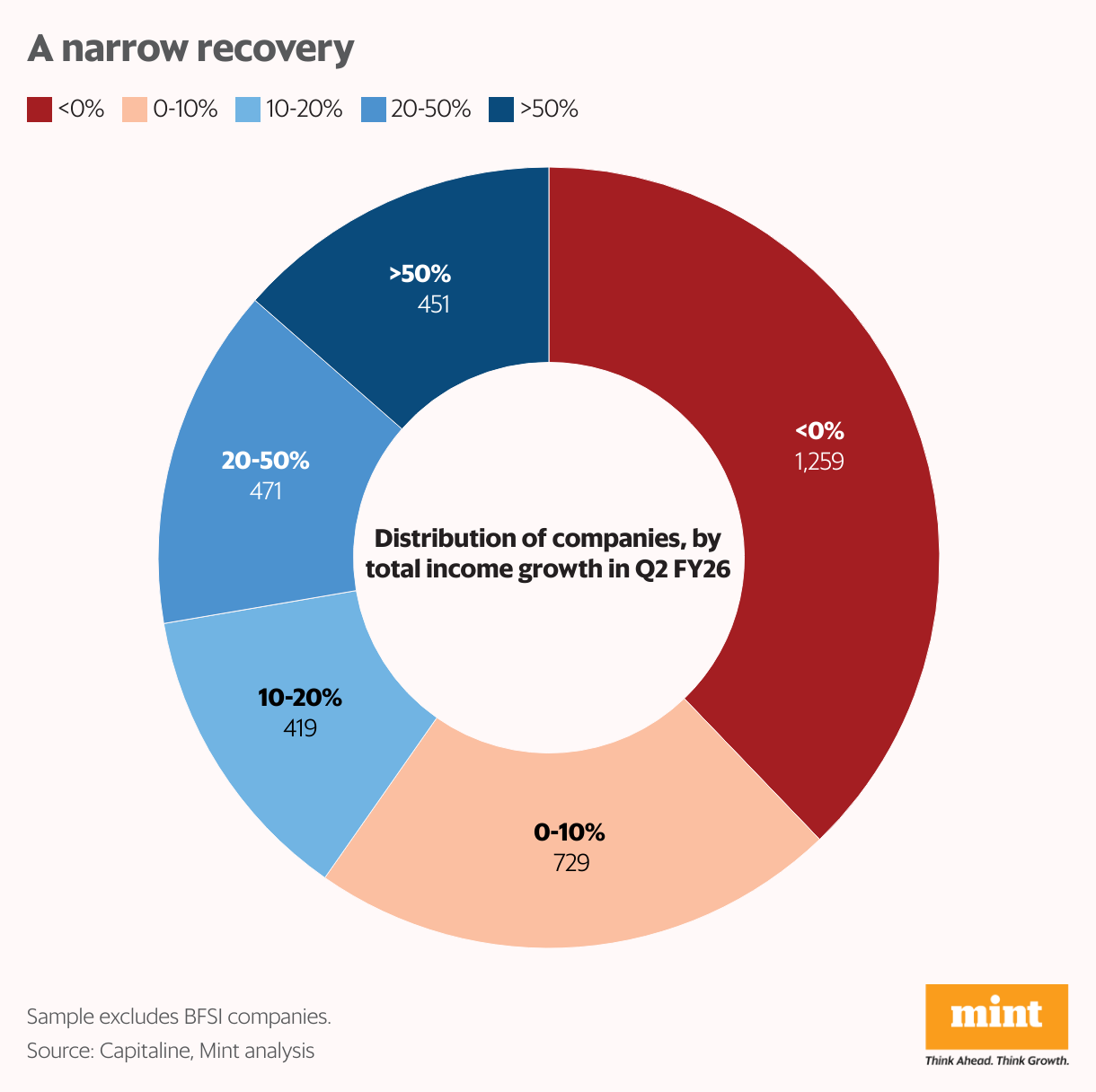

Actually, mint The analysis shows that around 38% of ex-BFSI firms saw a decline in total revenue on an annual basis in the second quarter of FY26; This rate is higher than the approximately 36% level in the 1st quarter. This was the largest share of companies reporting revenue declines in at least five quarters.

Approximately 22% of companies saw total revenue growth of only 0-10%; This indicates a lot of weak-to-medium performance. The other 13% grew by 10-20% year-on-year, reinforcing that the recovery was driven by many modest growers rather than a broader acceleration in income. Meanwhile, approximately 27% of firms achieved major revenue growth of over 20%.

More importantly, the share of fast-growing companies has been shrinking over the last five quarters, with more and more companies drifting towards the below-10% or negative growth group. This shows that while total BFSI ex revenue reached its highest level in nine quarters, the recovery remains concentrated among a small group of outperformers.

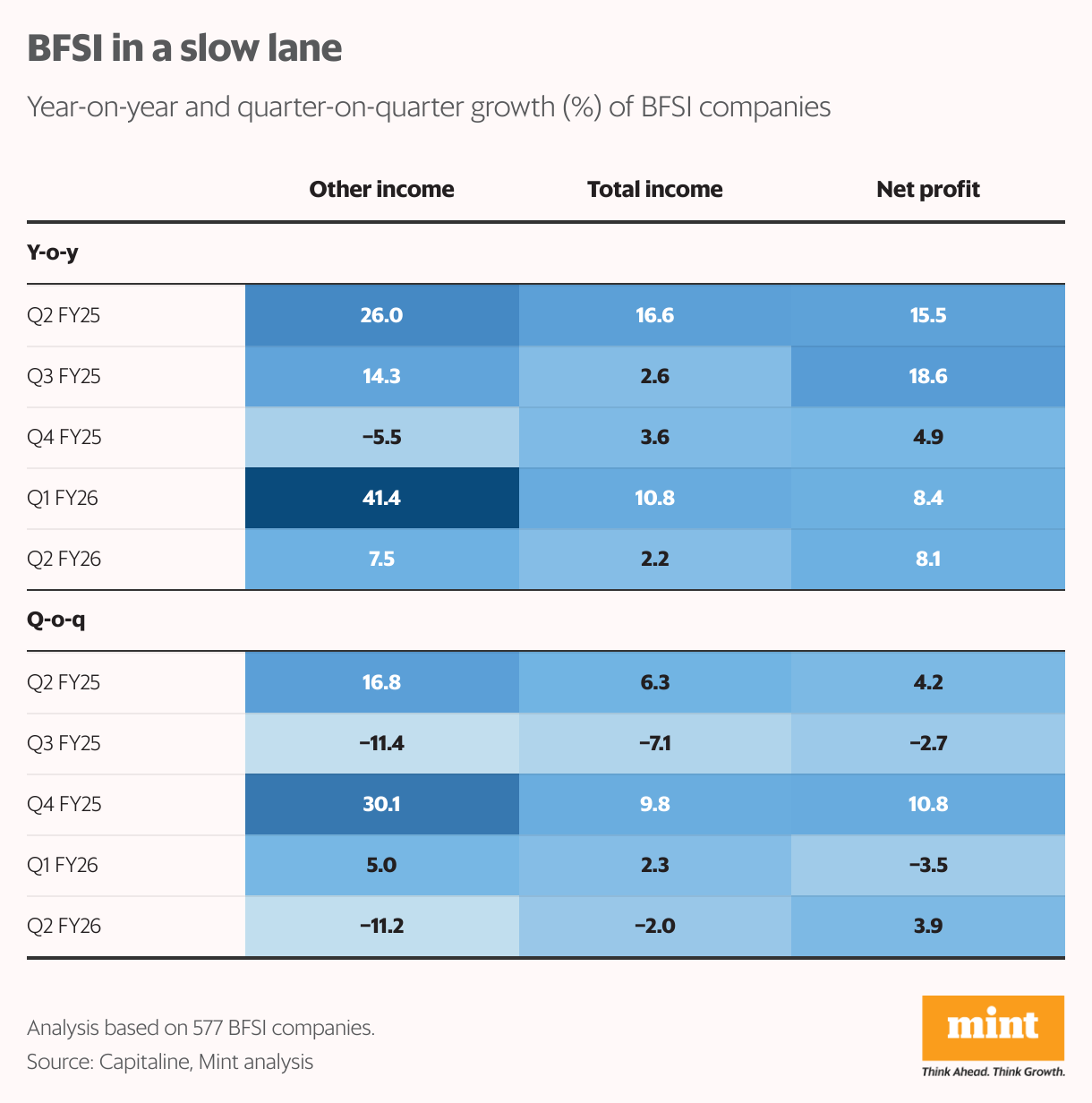

BFSI struggles

Jain noted that an uneven recovery can be seen even in BFSI. “Even as system loan growth remained close to 10 percent, major banks managed to increase (loan) advances by 14-15 percent on an annual basis,” he added.

The analysis showed BFSI’s total revenue grew just 2% year-on-year, its slowest pace in nine quarters, while non-core revenue grew a modest 7.5%. This limited operating momentum slowed net profit growth to 8%, well below the nine-quarter average of 15.5%.

In turn, the picture became even more gloomy. Although the segment still managed to turn a 4% profit, non-core revenues fell 11% in the second quarter, reducing total revenue by 2% from the previous quarter.

BFSI earnings remain weak Rural incomes and weak mass market consumption have slowed rural credit and personal credit growth. Meanwhile, cautious underwriting and muted private capital spending continue to constrain overall credit demand, experts say.

Rahul Gupta, chief operating officer of Ashika Securities Brokerage, said the segment also experienced a 30-80% decline in treasury revenue compared to the previous quarter, which negatively impacted BFSI’s non-core revenue.

“The sharp market-to-market headwinds of the first quarter subsided in the second quarter, with bond yields remaining stable or slightly rising,” Gupta said. “With the second quarter being the trough, treasury earnings should improve throughout the second half, supported by the RBI’s expected 25-50 basis point rate cut.”

Comeback hopes

Centrum Broking’s Jain said the market was pricing in another 25 basis point rate cut due to persistently weak inflation. In anticipation of a festive revival in consumption He added that GST cuts have fully come into effect and sentiment has strengthened.

Nifty 50 is trading just below its all-time high of 26,277 since September 2024. Jain said the stability in Q2 earnings ratings also improved the risk-return pattern. However, he added that with expectations already falling sharply in the last two quarters, more companies are simply meeting estimates rather than beating them. Jain expects Nifty earnings to grow by around 12% in FY26.

TrustLine Holdings’ Giri said the second quarter marked a solid turnaround in underlying earnings momentum. “While H2 looks stronger, real and widespread earnings growth is expected in FY27.”