Borrowers back to square one as likely rate hike looms

Mortgage holders are expected to be hundreds of dollars worse off each month than at the beginning of the year, as the Federal Reserve prepares to impose its third consecutive interest rate hike on borrowers.

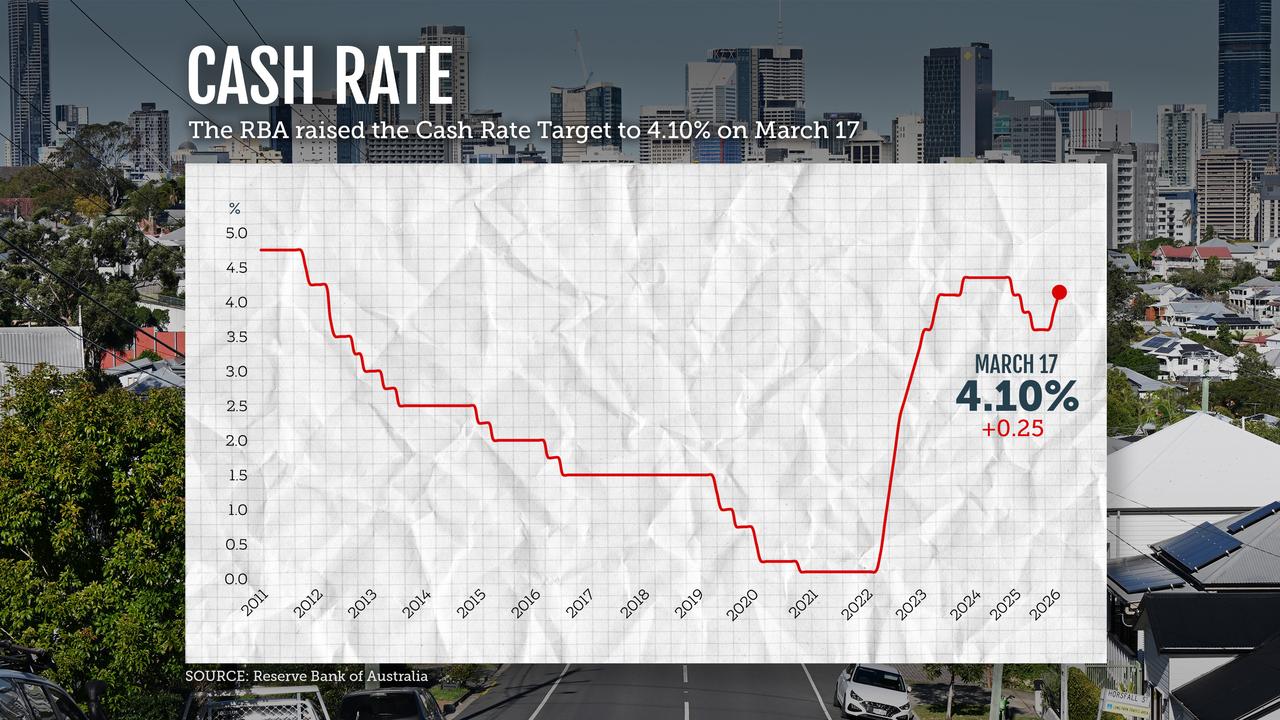

Financial markets were pricing in the chance to raise the central bank’s cash rate by more than two-thirds by 25 basis points on Tuesday after headline inflation rose to 4.6 per cent in March.

Rising fuel prices caused by the US-Israeli war with Iran further increased the central bank’s inflation problems.

The price increase was already well above target before the conflict broke out and threw global energy markets into chaos.

Economists at Commonwealth Bank, NAB, ANZ, Westpac, AMP, Deutsche Bank, Challenger, JP Morgan, HSBC and Citi all predict Reserve Bank governor Michele Bullock will announce an increase.

This will bring the cash rate back to the peak of 4.35 percent before the Federal Reserve’s short-term interest rate cut in 2025.

For the average borrower with a $600,000 mortgage, three consecutive increases since February will add up to more than $270 a month cumulatively in interest repayments.

Citi economists Faraz Syed and Josh Williamson expect the board to be less divided than at the March meeting, when only five of nine members voted in favor of the raise.

“The transition from inflation has been stronger than expected, with construction costs, international airfares and food prices expected to rise in coming quarters, whether or not a Middle East peace deal is reached tomorrow,” the pair wrote in a research note.

The Central Bank’s Monetary Policy Statement, which includes updated economic forecasts of the bank staff and gives clues about the future path of interest rates, will also be closely watched.

IG market analyst Tony Sycamore expects inflation forecasts to rise in the near term, then be cut further, to reflect slowing economic growth as a result of higher oil prices and interest rates.

Despite the oil shock, spending remains resilient for now, according to payments data from the Commonwealth Bank.

CBA economist Ashwin Clarke said although spending growth was expected to soften over the remainder of 2026, there was no sign that the recent sharp downturn in sentiment had materially changed households’ spending decisions.

Expenditures increased by 6.7 percent in the first four weeks of April compared to the same period the previous year; But while gas station spending rose, travel, retail and dining out were softer.

Broader discretionary spending appears to be holding up relatively well, according to transaction data from National Australia Bank.

NAB economists Gareth Spence and Jessie Cameron said rising construction costs were likely to contribute to a rise in housing inflation.

Construction materials prices were already high following the post-COVID-19 pandemic inflation spike, and the war in the Middle East will put further pressure on a wide range of products due to higher transportation, energy and input costs, especially plastics such as PVC pipes.

Housing approvals were improving before the conflict, the Australian Bureau of Statistics reported on Monday; Although the number of approvals decreased by 10.5 percent month-on-month, the trend rate increased to 17,657 in March.

“However, headwinds are increasing as higher interest rates and rising construction costs weigh on the sector,” CBA economist Lucinda Jerogin said.

“With the announcement of construction material cost increases, we expect new housing cost inflation to increase in the coming months.”

Australia’s Associated Press is the beating heart of Australian news. AAP is Australia’s only independent national news channel and has been providing accurate, reliable and fast-paced news content to the media industry, government and corporate sector for 85 years. We inform Australia.