Spending without thinking is a risk with unlimited contactless cards

Kevin PeacheyLiving Reporter Cost And

Tommy LumbyJob data journalist

Getty Images

Getty ImagesAcademicians are likely to increase spontaneous expenditures if the boundary on the contactless cards is completely increased or scrapped.

Currently, the need to print a four -digit PIN for purchases over £ 100 is reducing the risk of debt fuel purchase by giving people a timely request about how much they pay.

At the beginning of this week, the UK’s financial regulator proposed to allow banks and card providers to identify or completely remove their limits. This makes it even more rare to enter a pin.

Banks and some BBC readers should be able to determine their contactless boundaries of consumers, because the discussions on the issue are prevented in the future of the year.

Is it careless or over -arranged?

Contactless payments have become a part of daily life for millions of people around the world.

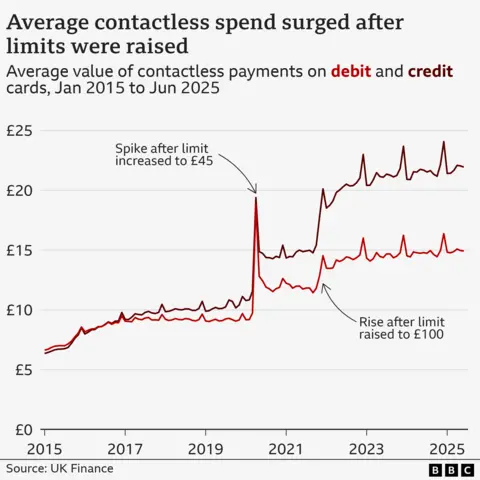

When introduced in the UK in 2007, the transaction limit was determined as £ 10. Since then, increases in the threshold, the pandemi at the time of the relatively large jumps in 2020, 45 £ 45, then in October 2021 to £ 100 £.

They caused fluctuations in average contactless expenditure.

Obviously, the average will increase, because more, higher value, purchases can be made through contactless without pin.

However, what is much more difficult to measure is whether people spend more often and larger amounts than they need to enter a pin.

Richard Whittle, an economist at Salford Business School, says that extra convenience for consumers can cost at cost.

“If this ease of payment leads to consumers’ spending without thinking, the probability of buying what they don’t really want or needs may be higher,” he says.

He says that there may be a certain problem with the credit cards that people spend money and accumulate debt. He believes that regulators should think if they have different rules for contactless credit cards than contactless debit cards.

Stuart Mills, a faculty member of the University of Leeds, says that Cash gives “visible and urgent feedback” about how much money you have, and is an “important friction point” to control a pin expenditures.

“The removal of such frictions, while offering some conveniences, they will see that more people have noticed that they spend more than they plan,” he says.

Both academics have brought this concern to the agenda before, but this is not only a theoretical argument.

Robert Ryan shopping in Sevenoaks town of Kent Market Told to BBC This gives me a little request to make sure that I am not spending much on my faucet-go “.

However, for many people, the truth is that under the pressure of the cost of living, rarely spend more than £ more than 100 at a time, so it has become contactless norm.

Research by Barclays shows that approximately 95% of all suitable in -store card transactions are contactless in 2024.

Terezai Takacs, who works in a florists in Sevenoaks, says that in the last few years, people have reduced expenditures like asking smaller bouquets.

Technology inheritance

Miss Takacs also states that most of the customers are now paying through the digital wallet on their smartphones.

Paying in this way has an unlimited payment limit due to extra safety features such as Thumbprints or Face ID.

Dr Whittle, spontaneous or reckless expenditure, which is likely to dilute the impact of upgrading the contactless card limit – especially young people pay by phone.

Some say it is delayed to scrape the contactless card limit, because people are much less relevant when they are accustomed to spending on a phone.

“Editor is finally growing up about how people pay,” Fintech Company Cashflow General Manager Hannah Fitzsimons says.

“Digital wallets on smartphones do not bound, then why the cards should be stuck in the past?”

If the contactless card limit would be increased or scrapped, Britain would comply with the rules in more and more than Europe’s and other advanced economies.

In Canada, the industry determines the level instead of regulators and is determined by providers in the USA and Singapore – the financial behavior authority (FCA) is a model that it wants to reproduce in the UK.

Banks are joining the regulator, but the UK Finance – Industry Trade Organ – “Core will be thoughtfully with security,” he says.

Personal choice

Banks and card providers that change the boundaries will be encouraged to allow customers to identify their own thresholds or close them completely on their cards.

“Lloyds, Califax and Bank of Scotland customers can already determine their own contactless payment limits in our applications – up to £ 5 – and we are definitely determined to maintain this flexibility – and we are definitely determined to maintain this flexibility.”

This option has the support of some BBC readers, viewers and listeners who have contacted us. Your voice, your BBC News.

36 -year -old from London told us: “The most important principle here is personal choice. I want to determine my own personal limit.

“This is my card and convenience and risk tolerance. Some banks do not allow it. This option should be provided to everyone.”

Others have concerns about security, saying that unlimited contactless cards will be more attractive to thieves and scammers.

‘Unlimited abuse’

No institutions warn that not everyone has digital skills to determine their own limits. In other cases, it can have a very serious impact on people’s lives.

Sam Smethers, General Manager of the surviving economic abuse, says that unlimited contact cards give unlimited economic abuse to the partners who control unlimited economic abuse.

“Unlimited contactless expenditures can provide free access to abusers to destroy the bank account of the bank.”

“This can leave without the money they need to escape from a survivor and to reach security and push them even more.”

He warns that he can accelerate slipping towards a cash -free society.

Cash is a life line for many surviving people, because it was the only way to escape from the abusers who could watch online transactions, store debit cards and close their bank accounts.

Additional reports by Andree Masiah