Profit without punch, India Inc’s Q1 report card in charts

The whole orbit underlines a fragile and unequal earning cycle. While relieving income contractions and more companies manage stable but modest gains, there was no real fist, as the real -high growth contradictory values remained unchanged.

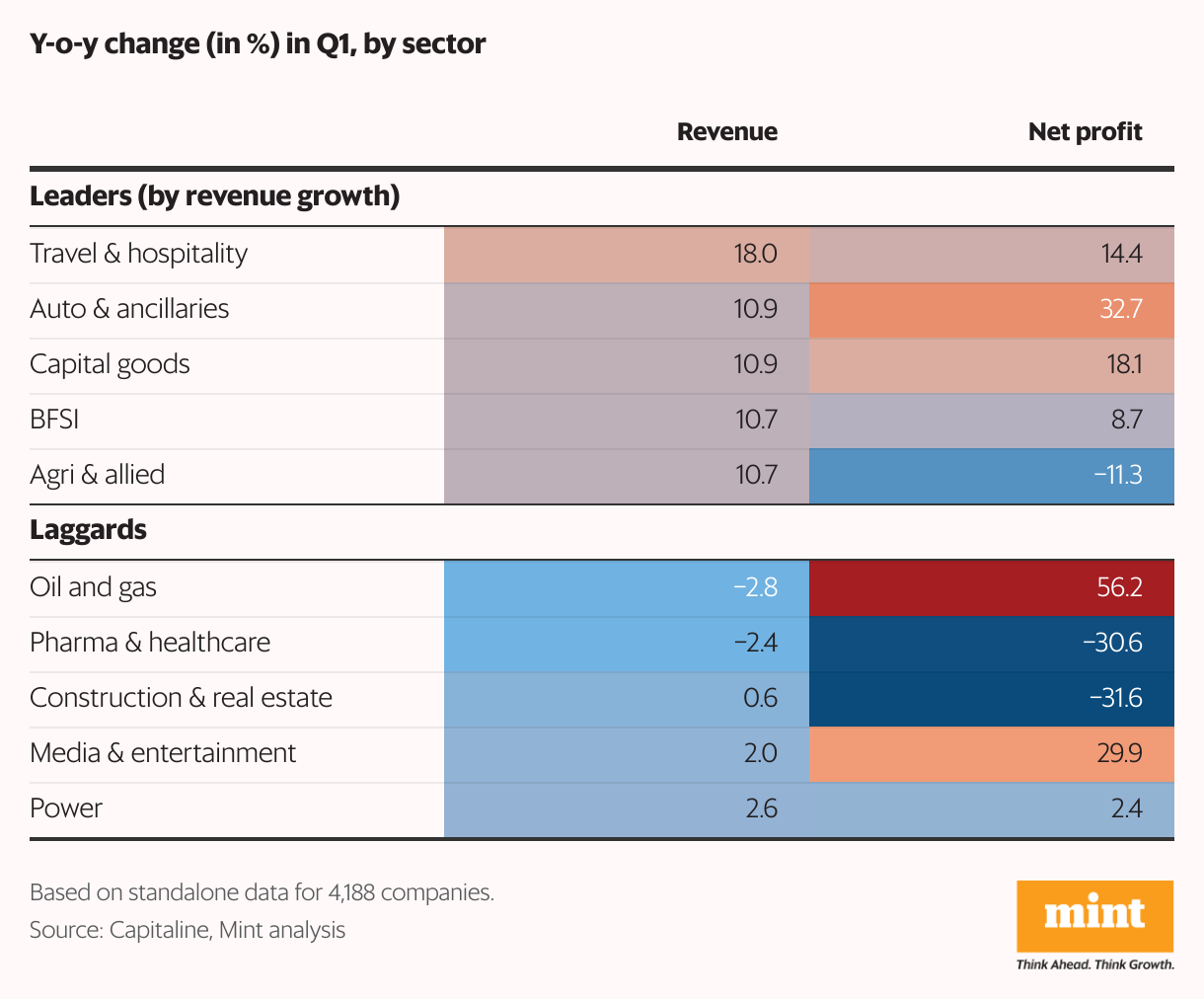

Sectoral prints eliminate the concept of structural power even more: travel companies continued at the summer request, oil marketing companies developed on cheaper crude oil, and automobile manufacturers earned from softer input costs.

Banks, Financial Services and Insurance Companies (BFSI) were balanced with stable revenues, decreased margins and increasing credit costs, and pharmaceutical and real estate companies faced sharp snow problems.

Ultimately, most of Q1’s profit flexibility leaned against the cyclic and cost -tail winds, which raised business margins to the highest level of one year, even when wage and interest invoices rise. Although it is difficult to revive a wider demand, early symptoms of rural consumption and a lower share of lost companies offer a light of hope.

However, with continuous decreases and rich values, the market is now demanding acceleration (volume, realization and execution) working on short -term treasury earnings and accounting elevators.

How did the story come about

The latest earning season appeared as a dramatic narrative with an opening action that left investors on the sidelines. Bellwethers’ first statements, such as Tata Consultancy Services, set a terrible tone that declares a flat income and warm profit growth on the market.

However, the second half changed in the second half of the profit, which was increased by Asia Paints and HDB financial services, respectively by Reliance Industries and HDFC Bank, respectively.

Momentum was maintained in the middle of the season with a long -awaited rise and a strong performance by the cement industry in consumer staples. Gradually, the highest -level growth of the India Inc reached the summit in early August. However, as the smaller and middle cover companies that create more losses report their earnings, India Inc’s income increase decreased at the fagot end of the earnings season.

Money Manufacturers

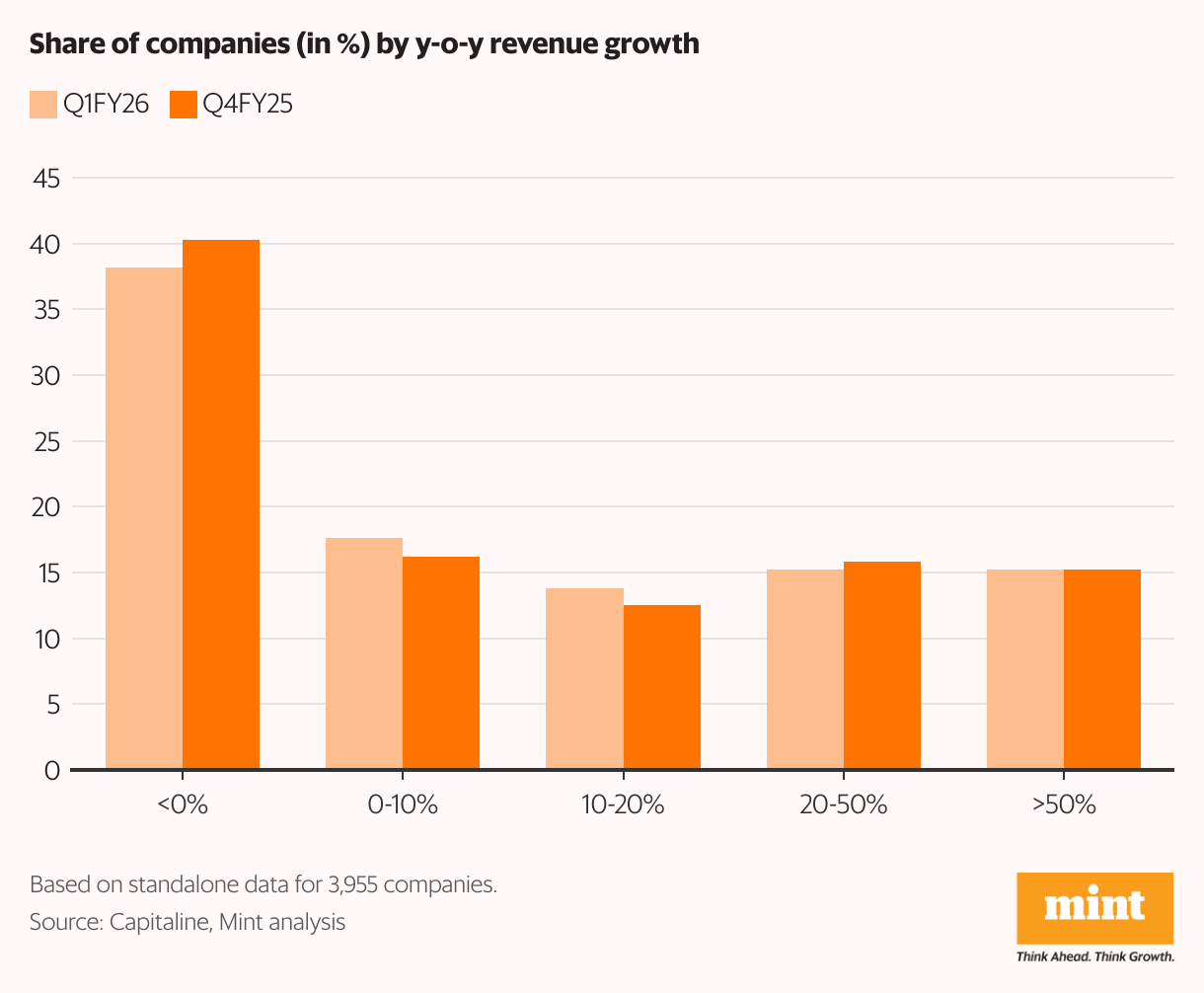

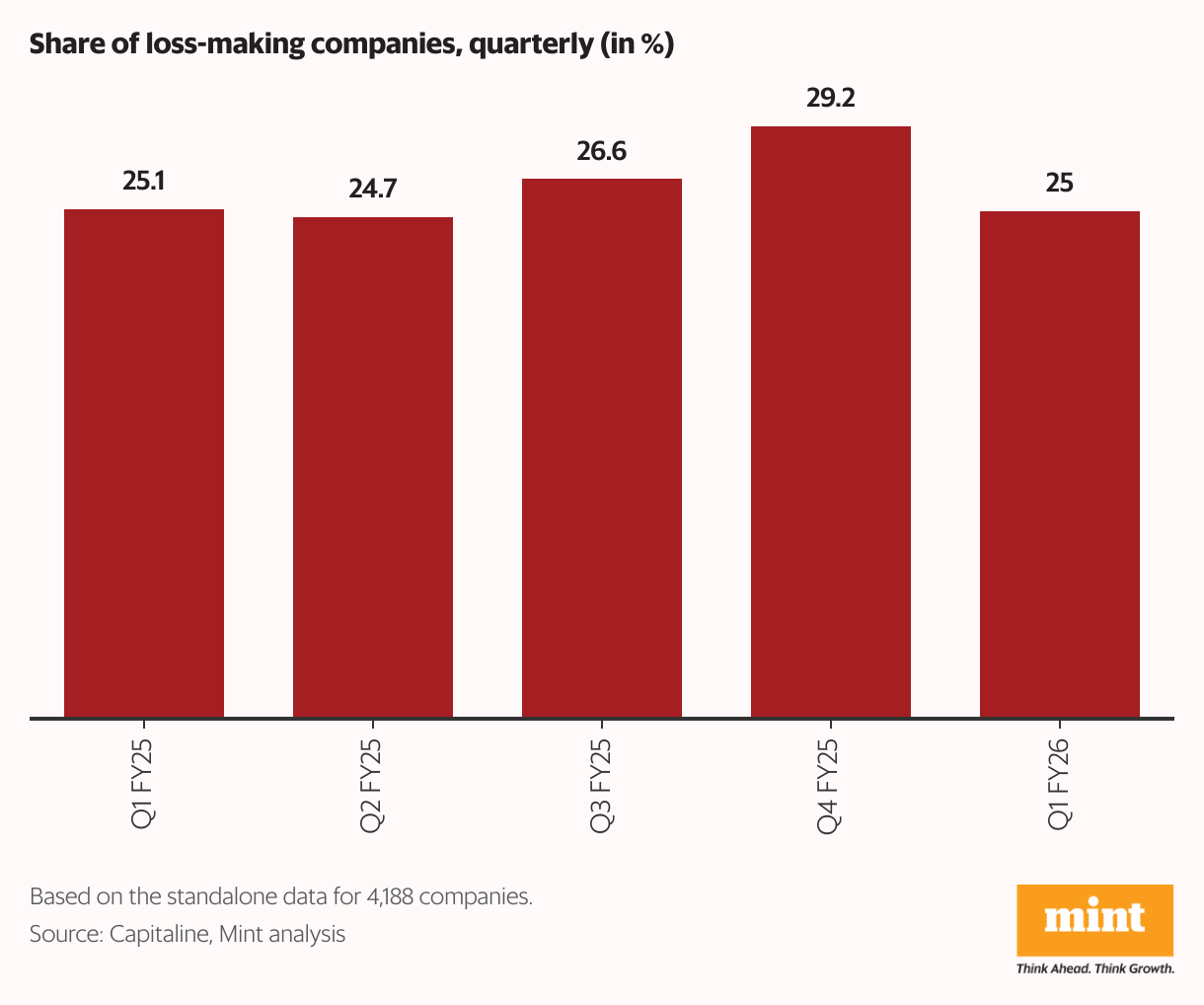

Even if the general results seem inanimate, the earnings season received a positive note: fewer companies reported that they are compared to the previous period. This shows that India Inc. found a tighter foundation.

Nevertheless, the rally showed width without biting; While the cohort of modest artists grew, the share of really strong winners (those with more than 20% volume growth) (growth of 50% growth) remained unchanged.

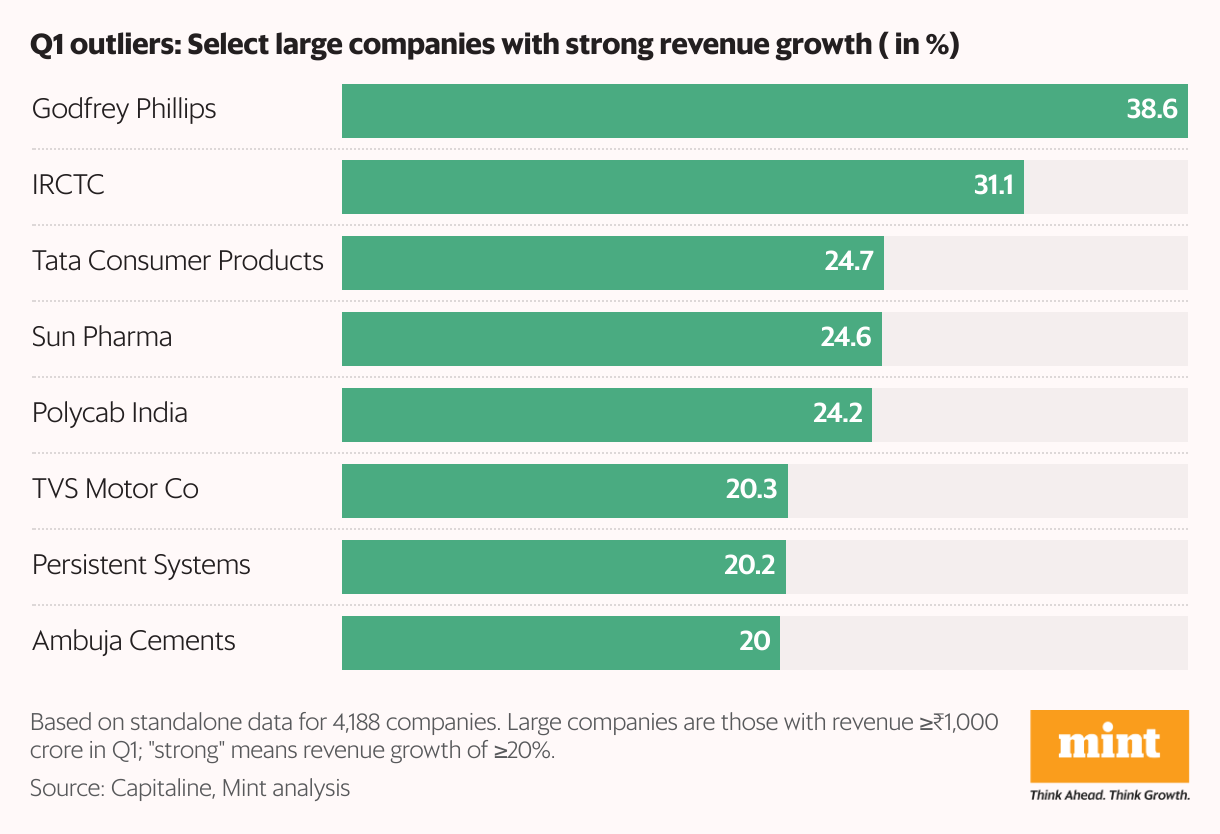

Nevertheless, a clutch consisting of large names such as Godfrey Phillips and Tata consumer products performed better due to consumer demand for premium goods. Similarly, polycab and ambuja cements used a solid cement demand to provide market trends such as widespread distribution of wires and cables, and a powerful upper line.

Optical illusion

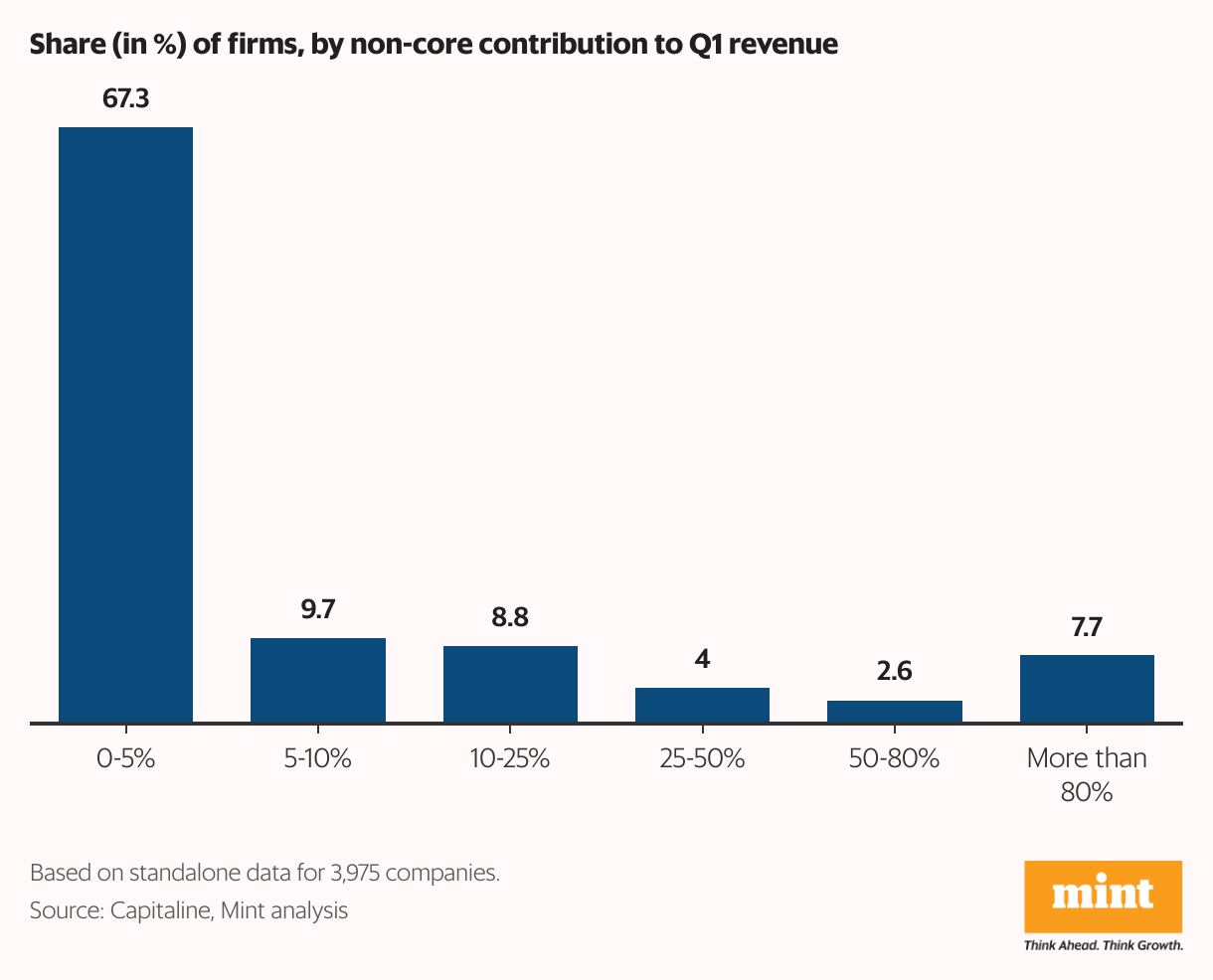

Despite the dominant business conditions, a clear model emerged: India Inc. It mainly produced its first quarter earnings from basic operations. However, when we look at it more closely, it reveals that someone from ten companies is roughly based on non -nuclear revenues.

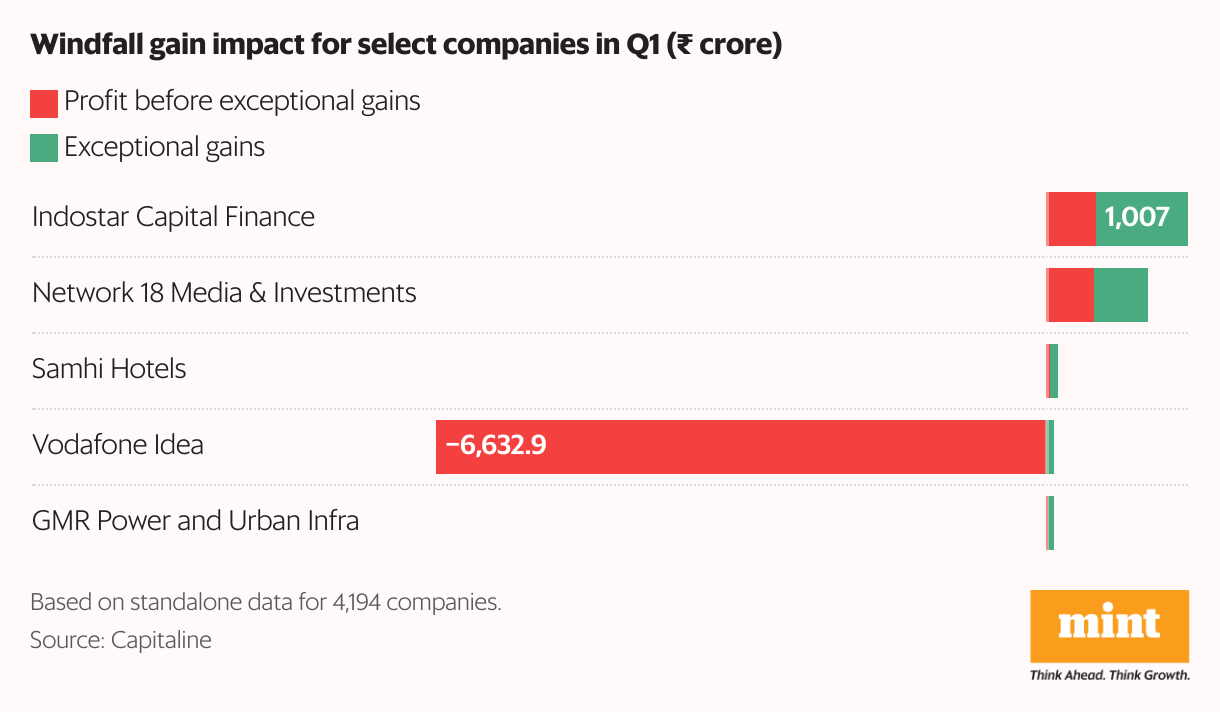

In fact, most of the remarkable achievements of the quarter were directed by one -time winds. For example, the upper line of the banking sector is supported by significant treasury income in the midst of warm credit growth. Certain companies such as Indostar Capital Finance and Network18 have also seen that their profits have increased from one-time activities and an asset sale and an accounting change. While these repetition increases illuminate the three -month picture, a structural recoil in India Inc’in earnings is still difficult.

Alleviating pressure

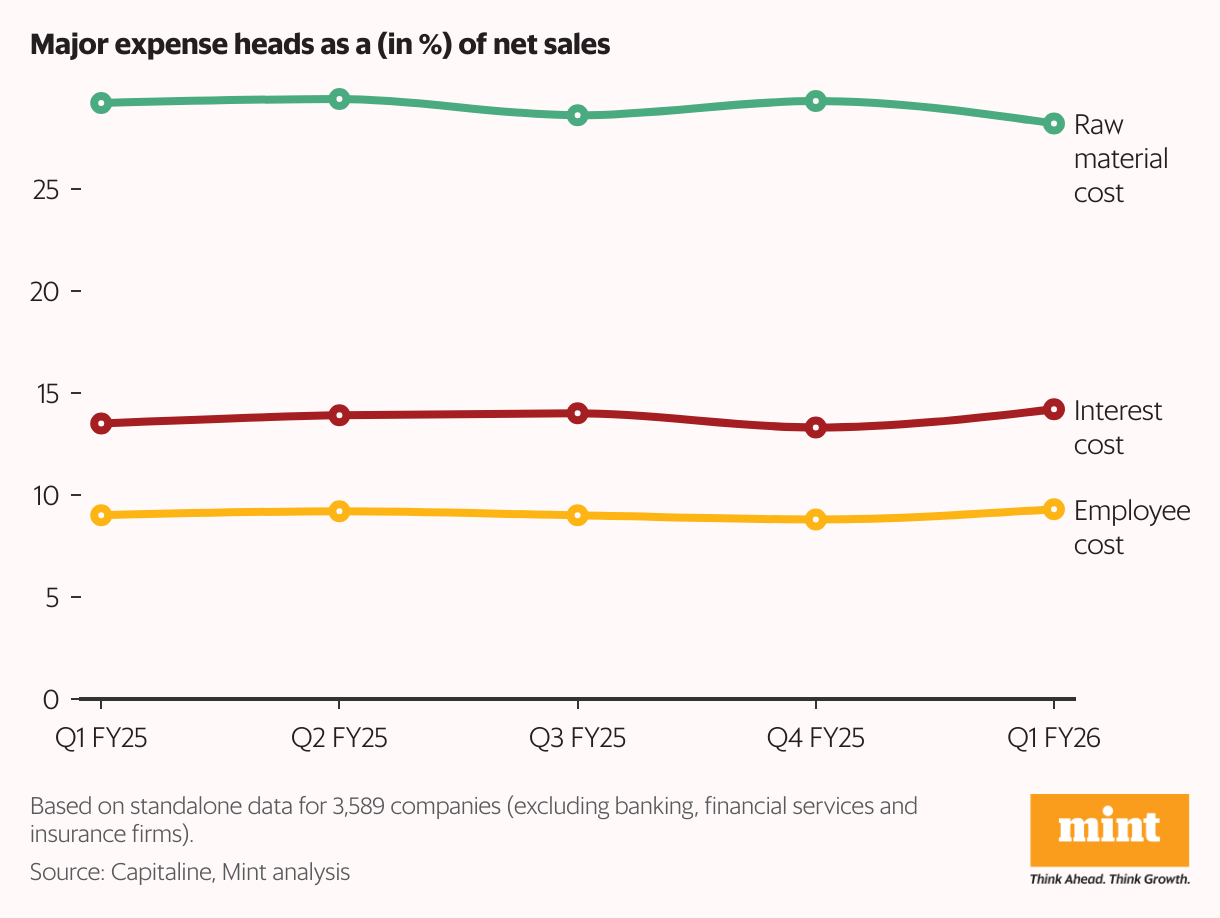

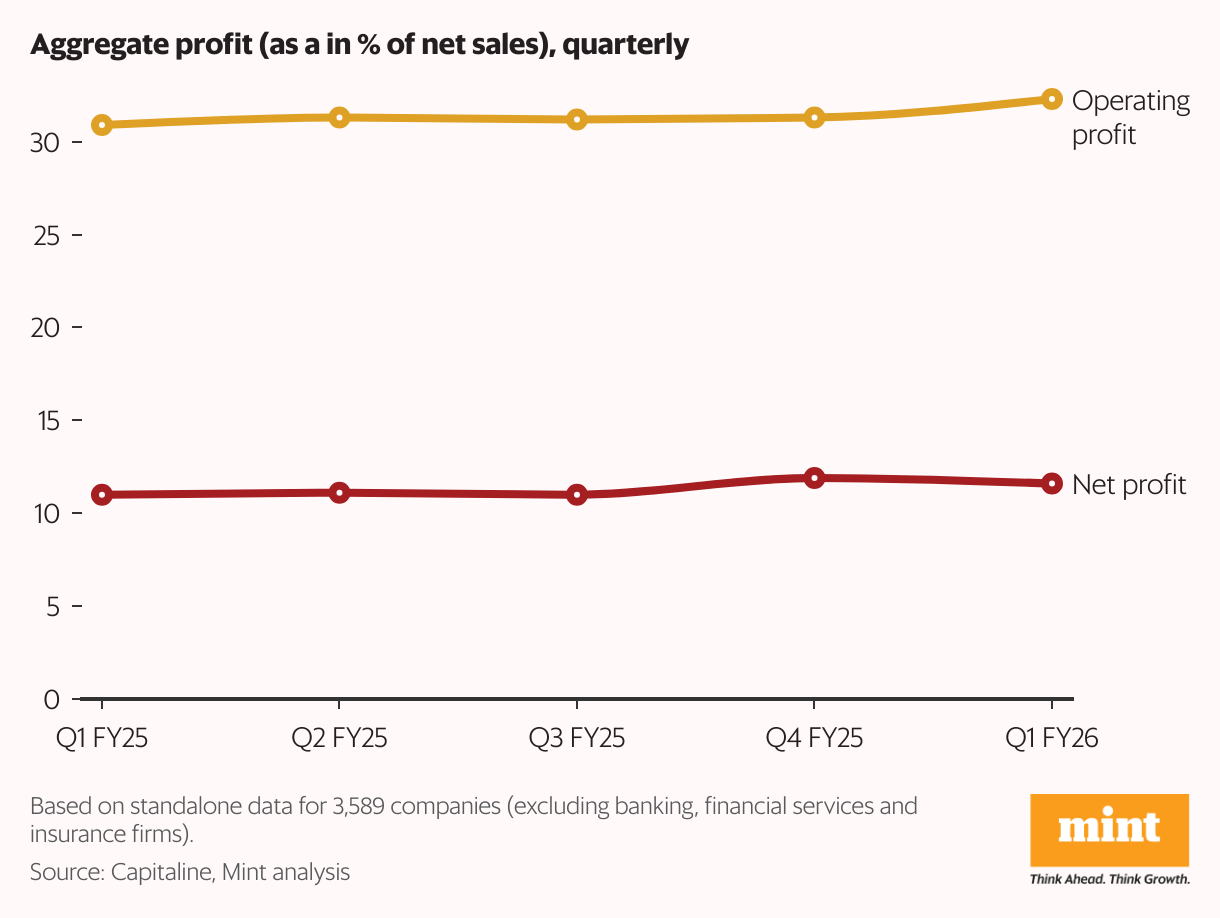

In a positive note, alleviating raw material costs increased Indian Inc.’s operating margins to the highest level of one year in the first quarter. Lower crude oil and metal prices, caused by the fear of a global demand slowdown, helped to reduce production costs despite weak senior growth and kept companies widely profitable. However, these gains were partially balanced with increasing employee and interest costs. As a result, although the net margins were strong, they could not reach the summit of the last quarter. However, experts warn that input-fold tail winds may disappear by the end of the year and that India Inc may arous suspicion of profit sustainability when there is no strong income backfire.

Mitigation of raw material costs increased India Inc.’s business margins to the highest level of one year. This helps companies to remain profitable despite the weak income increase, while increasing employee and interest costs partially balanced gains. Experts warn that these tail winds can soon be lost and that they can arous doubt of profit sustainability without a stronger income backfire.

How did various sectors progressed

Sectoral tendencies show that commodity winds float many sectors and pillow the effect of weak upper line growth. For example, the oil and gas sector was the biggest delay in the first quarter income growth. Nevertheless, lower raw prices also noted the sharpest profit growth of major oil marketing companies to increase the refining and marketing margins.

Meanwhile, the travel and hospitality industry reported the highest increase in income managed by the demand for free time.

On the other hand, the BFSI provided stable revenue increase, but increasing credit and financing costs and net interest margins focused on profits. This shows that the India Inc’s 1st quarter gain story does not have a wider charm, and that a real sustainable recovery has not yet emerged.

Silver Primer

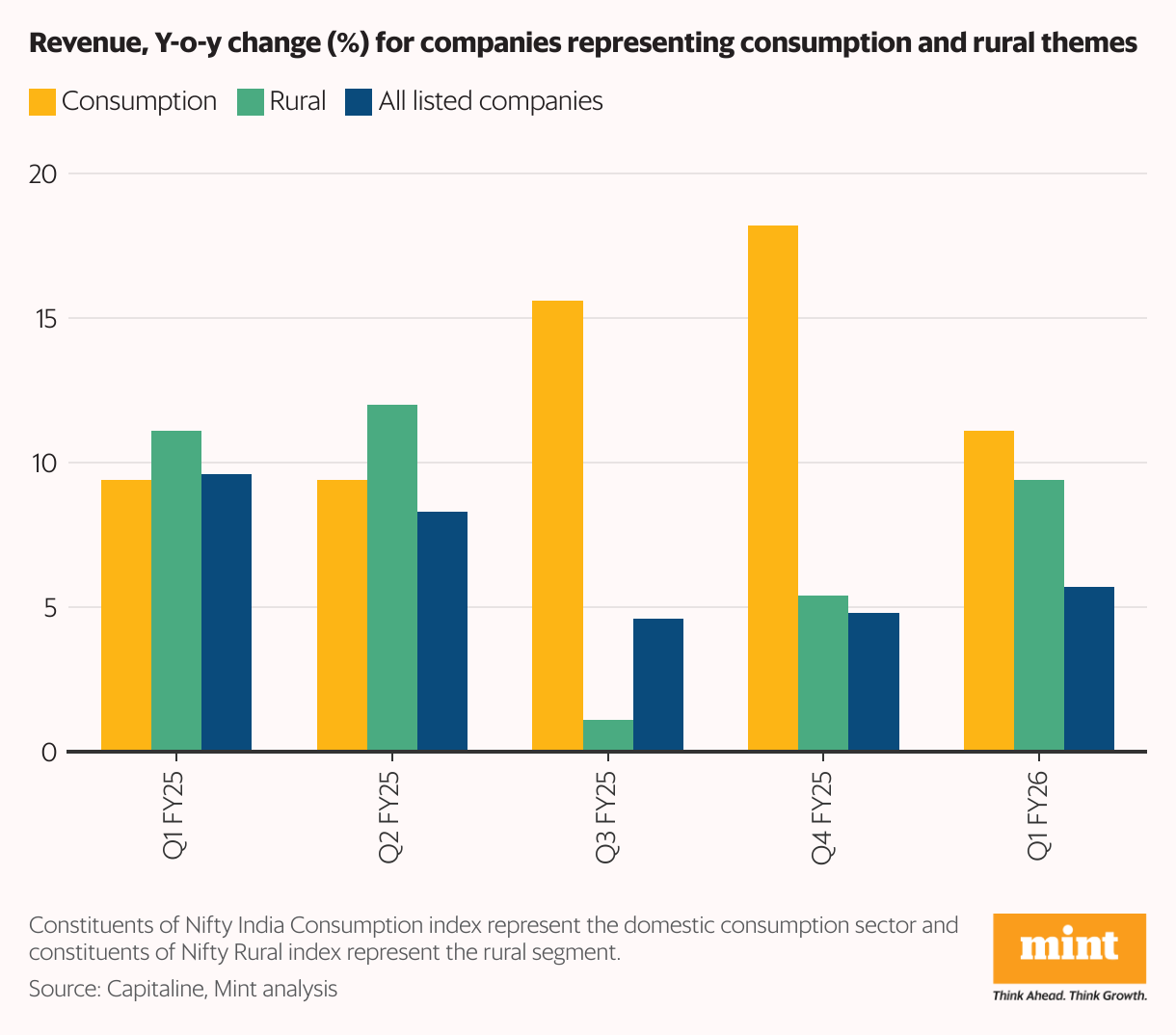

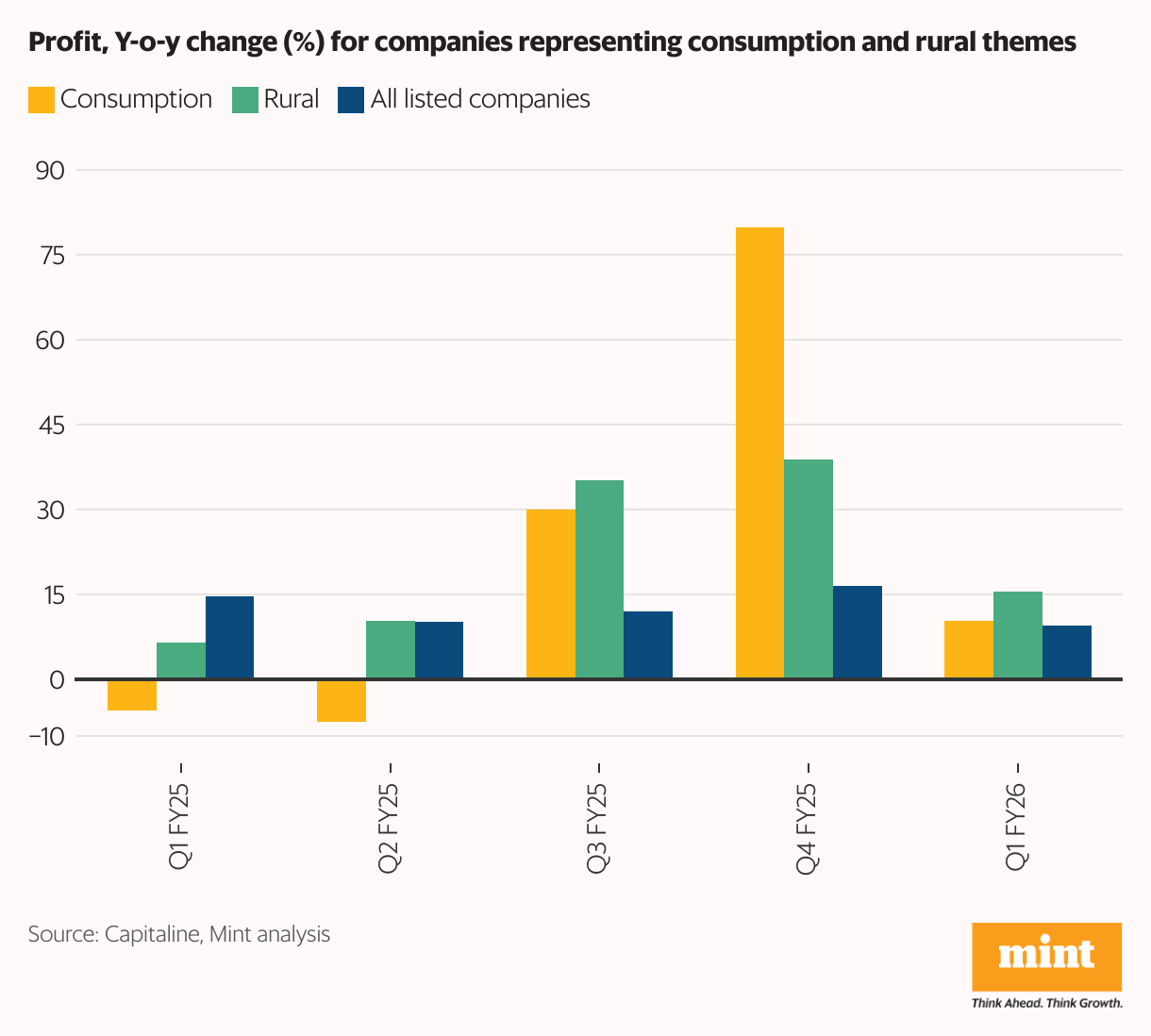

In encouraging way, especially green consumption from a flexible rural economy, revival exiles remove expectations for a second half of the 26 financial year. Rural-oriented companies, the wider market has left behind the growth of earnings-if there are monsoons and income, a promising sign.

The quarter also saw wider profitability gains, and the share of lost companies fell to three thirds in the second quarter. However, the view of consensus is that India Inc.’s gains have not yet hit the bottom and that a real momentum is only likely to return later in the financial year.

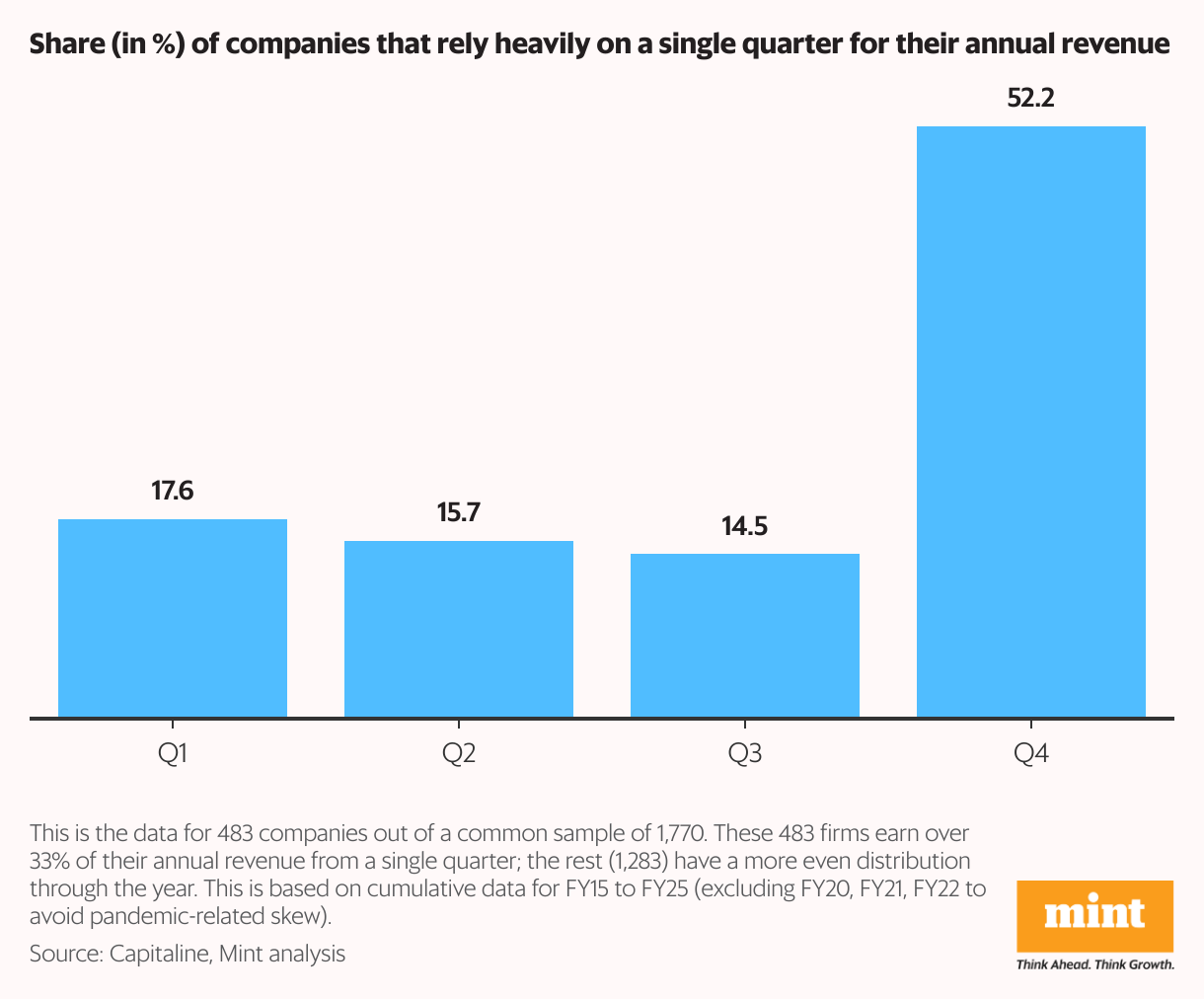

Seasonal riches

However, for a large area of India A.Ş., in the quarter, the fiscal year is not a marathon-a high-bet gambling in a single quarter. For these companies, a weak seasonal demonstration may mean a lost financial year, which can allow them to look at the whims of festival calendars, weather conditions and capital expenditures.

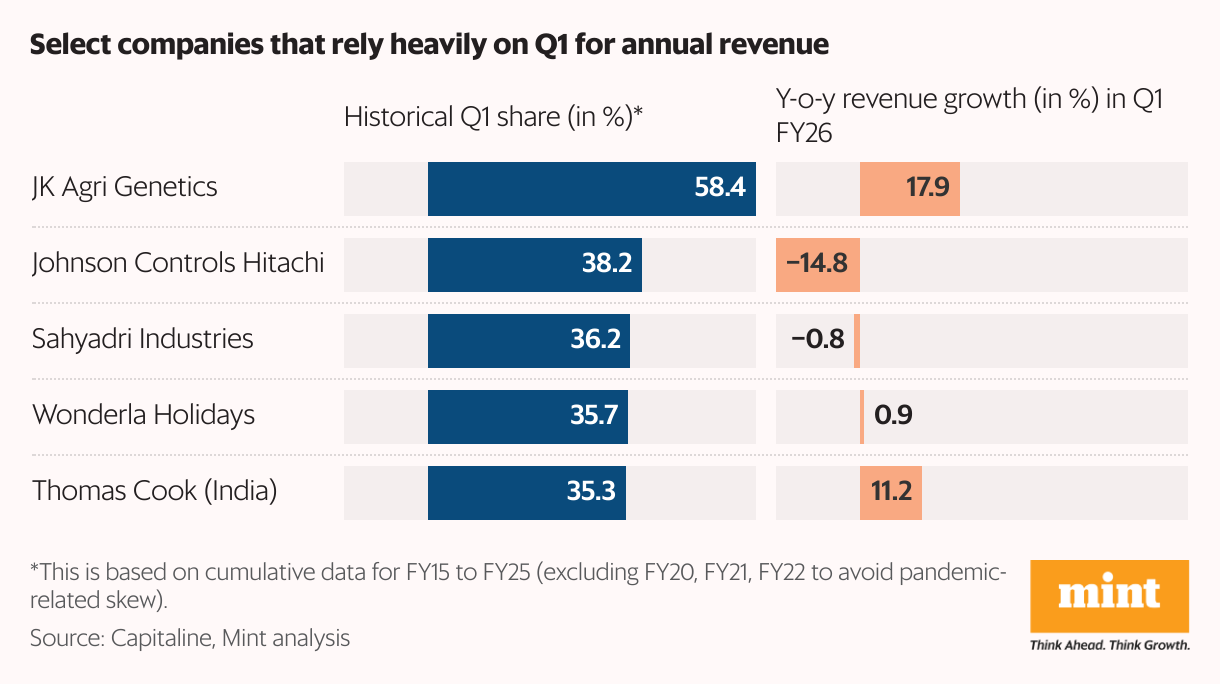

The effects of seasonality were clearly seen in Johnson Controls-Hitachi, a company that has historically achieved a significant portion of its income from the first quarter summer heavy air conditioning sales.

However, a significant decrease in income in this quarter due to early monsoon may force aggressive sales tactics that may harm the company for the rest of the year. On the Flip side, the expectations of a favorable monsoon and a better Kharif cycle presented tail winds to the upper line of JK Ağri Genets and traditionally relying on the first quarter for their earnings.