Where are UK mortgage rates heading in 2026 as Iran war continues to impact?

For borrowers preparing to seek new mortgage deals, the first quarter of 2026 has revealed how quickly market conditions can change, turning from encouraging to unstable.

Just last month, companies priced in the potential for a cut to the Bank of England’s base rate as various lenders competed to offer attractive terms.

But it’s a very different story today, with hundreds of home mortgage products withdrawn in March, partly due to the impact of the Iran war on the UK economy, but also because swap rates rose as speculation about interest rate rises increased.

Ryan Brailsford, sales director at lender Pepper Money, says: “Rising energy prices and geopolitical tensions have increased the swap rates lenders use to price fixed-rate mortgages, and a number of high street lenders have already responded by increasing rates.” According to Moneyfacts, Average mortgage rates rose above 5 percent in March, the highest number in seven months, and are now hovering around 5.5 percent as we approach April.

There are a variety of directions costs can go, making forward planning difficult for consumers, with tensions in the Middle East contributing to what Craig Fish, founder of broker Lodestone Mortgages, calls “the most unpredictable forecast environments in recent years.”

So what do real estate and loan experts think the outlook for mortgage rates could look like for homeowners and first-time buyers in the second and third quarters of 2026? Any advice for households?

Interest rate debates and new agreements are ahead

The Financial Conduct Authority estimates that around one million fixed-rate mortgage deals will expire between April 1 and the end of September.

This will likely see a significant amount of new deals sought. Additionally, those stepping onto the property ladder for the first time will also shop for loans.

Get a free partial share of up to £100.

Capital is at risk.

Terms and conditions apply.

ADVERTISING

Get a free partial share of up to £100.

Capital is at risk.

Terms and conditions apply.

ADVERTISING

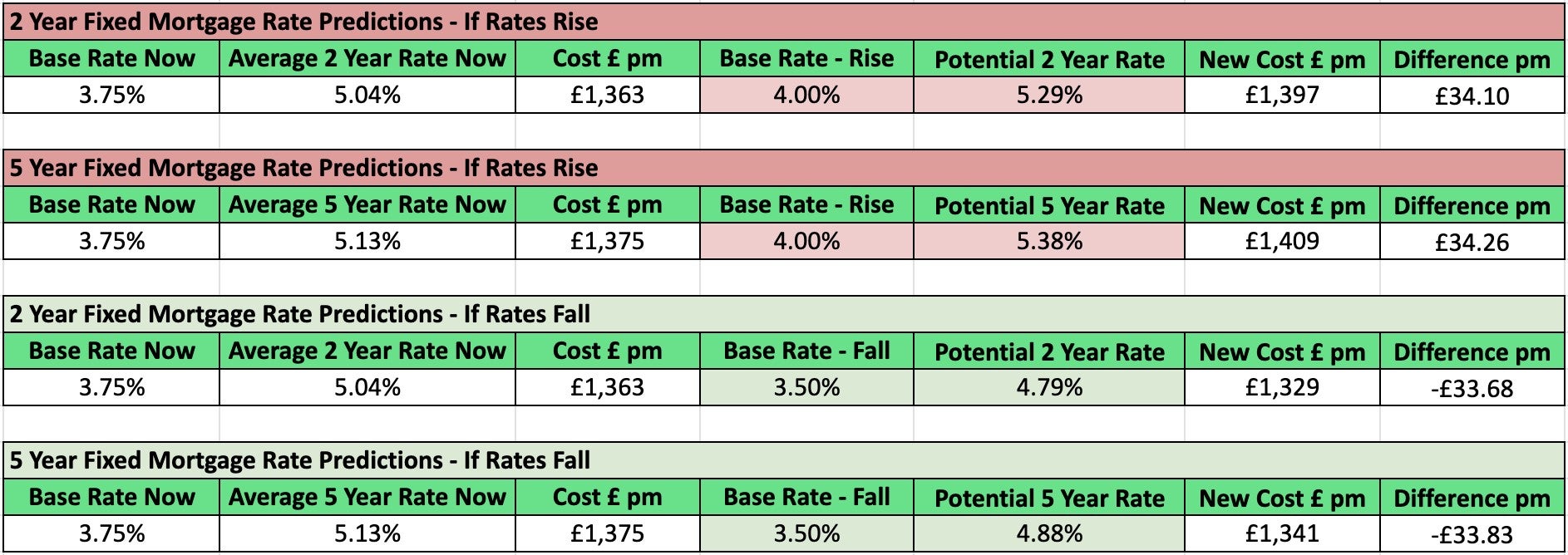

The Bank of England interest rate is currently 3.75 per cent and before the latest conflict in the Middle East forecasters had predicted a rate cut in March. However, this situation turned into a vote as rising oil prices brought with it the threat of higher inflation.

Jonathan Samuels, managing director at specialist lender Octane Capital, says: “Mortgage rates can change much more quickly than many borrowers realize because they are influenced not only by the Bank of England base rate, but also by wider economic sentiment and global events.”

The chart below from Octane Capital outlines an estimated comparison of base rate and subsequent mortgage rate scenarios if the conflict in Iran continues into the summer and leads to a rate hike, or ends earlier and leads to a rate cut later in the year.

Lodestone Mortgages’ Fish says: “If energy prices remain high over the coming months, inflation will become stickier than the Bank of England hopes, reducing both the scope and appetite for further base rate cuts.”

But he adds that if the conflict stabilizes, “the UK’s picture of weak growth and rising unemployment still gives the MPC good reason to make cuts, and cuts remain reasonable until September.”

We look forward to 2026

As of March 4, the average two-year fixed-rate mortgage rate across all LTVs was 4.82 percent, and the average five-year fixed rate across all LTVs was 4.94 percent, according to Moneyfacts data.

To give you a snapshot of what the industry currently thinks mortgage rates might look like at the end of the third quarter, around September. Independent asked five housing and credit experts for their opinions.

The average two-year fixed rate by the end of September could be 4.7 per cent and the five-year rate could be the same, according to average figures from forecasts provided by representatives from Jackson-Stops, JLL, Lodestone Mortgages, Pepper Money and SPF Private Clients.

Participants emphasized that it is difficult to make predictions, and some made predictions that did not foresee long-term tension in the Middle East..

Nick Leeming, chairman of estate agents Jackson-Stops, says: “Although we expected minor downgrades throughout 2026, the international conflict and geopolitical environment has changed radically, so it is very difficult to make any predictions.”

Looking at the longer-term picture, Marcus Dixon, UK housing research director at estate agency JLL, says current rates, despite recent increases, “remain more competitive than borrowers could have gotten at this time last year, which we think will bring more buyers to the market in 2026.”

Sharief Ibrahim, head of housing at real estate consultant CBRE, says: “The Bank of England may struggle to start easing interest rates due to inflation-related risks. However, our latest housing forecasts point to a relatively stable outlook for mortgages over the next 18 months. None of these point to dramatic swings, but while rate cuts may not come as quickly as some hope, they do suggest the outlook for borrowers is slowly and quietly improving.”

What should consumers consider doing?

Paula Higgins, managing director of property consultancy site HomeOwners Alliance, says it makes sense for clients to work with a mortgage broker who can monitor the market.

The broker can “help you find the right deal for you, set a rate upfront, and keep it under review in case a better option arises before you complete.”

Mark Harris, managing director at mortgage broker SPF Private Clients, says we could see lenders increasing mortgage rates to reflect higher Swaps if they continue to rise, “so borrowers planning to take out a fixed rate mortgage in the next few weeks or months may want to secure a product now.”

Harris adds: “This will give you peace of mind and if rates have fallen when you come to get the mortgage then you should be able to switch to a cheaper deal. But if rates have risen you’ll be glad you made the move when you do.”

When investing, your capital is at risk and you may get back less than you invested. Past performance does not guarantee future results.