Four years under Tata, Air India still in recovery mode. How does it stack up against IndiGo?

But even without the tragedy, data shows that Air India and its low-cost subsidiary Air India Express are growing more slowly than their main rival, IndiGo, and are far from challenging its dominance.

Domestic air pockets

India’s domestic aviation market has expanded steadily. The year the Tatas acquired Air India was still a period of recovery after covid-induced lockdowns, but 2023 saw around 152 million passengers on domestic flights, rising to around 161 million in 2024. Forecasts for 2025 show 165-170 million passengers.

Air India Express has shown steady growth, surpassing 10% passenger share for the first time in 2025. However, Air India’s domestic share fell following the frequency cut on certain routes following the crash in June. Meanwhile, IndiGo faced operational challenges due to pilot shortage under new regulations.

A clearer long-term view emerges by comparing market share between 2022 and 2024. During this period, the Air India duo gained 4.2 percentage points, while market leader IndiGo added 5.9 points on a larger base.

international turbulence

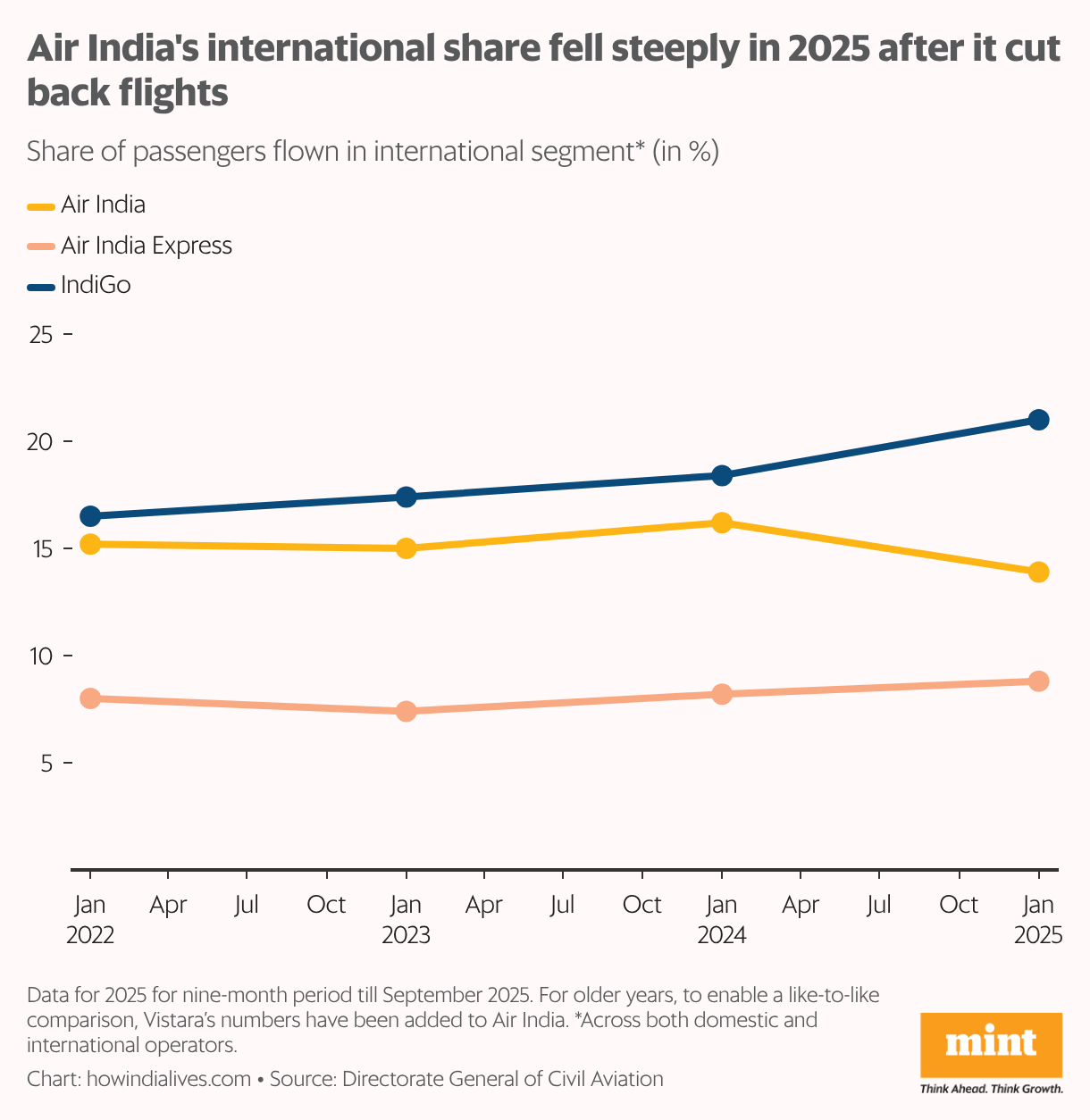

Similar trends were seen in the international segment. The number of passengers increased from 28.4 million in 2023 to 32.7 million in 2024. It is expected to reach 36 million in 2025. The total market share of Indian carriers currently stands at around 46%.

Air India reduced capacity on some long-haul routes following the plane crash in 2025, resulting in a significant decline in its share in 2025. Here too, a more accurate comparison is between 2022 and 2024, when the Air India duo gains 1.2 percentage points in passenger share, while IndiGo gains 2 percentage points.

Distance is another variable in the international segment. Air India operates wider-body aircraft that travel longer distances and have higher seating capacity. Therefore, its share in passenger revenues is higher than its passenger share. For example, among Indian airlines in 2024, Air India had a passenger share of 35.9% while it had a share of 53.1% in passenger-kilometres.

aging fleet

The plane crash in June 2025 was a setback for Air India. It is in the midst of an ambitious, multifaceted five-year transformation called Vihaan.ai, which begins in September 2022. Key pieces of this plan include purchasing new aircraft, retrofitting old ones, integrating multiple airlines, expanding to new routes, adding more operational staff and investing more in other building blocks such as training and maintenance.

It placed a multi-year order for 470 new planes from both Boeing and Airbus in 2023 and added 100 more in 2024. However, its deliveries lagged behind IndiGo. Boeing delivered 26 aircraft to Air India in 2024 and 15 in 2025. Meanwhile, Airbus has delivered 49 aircraft to IndiGo in 2025, almost one a week.

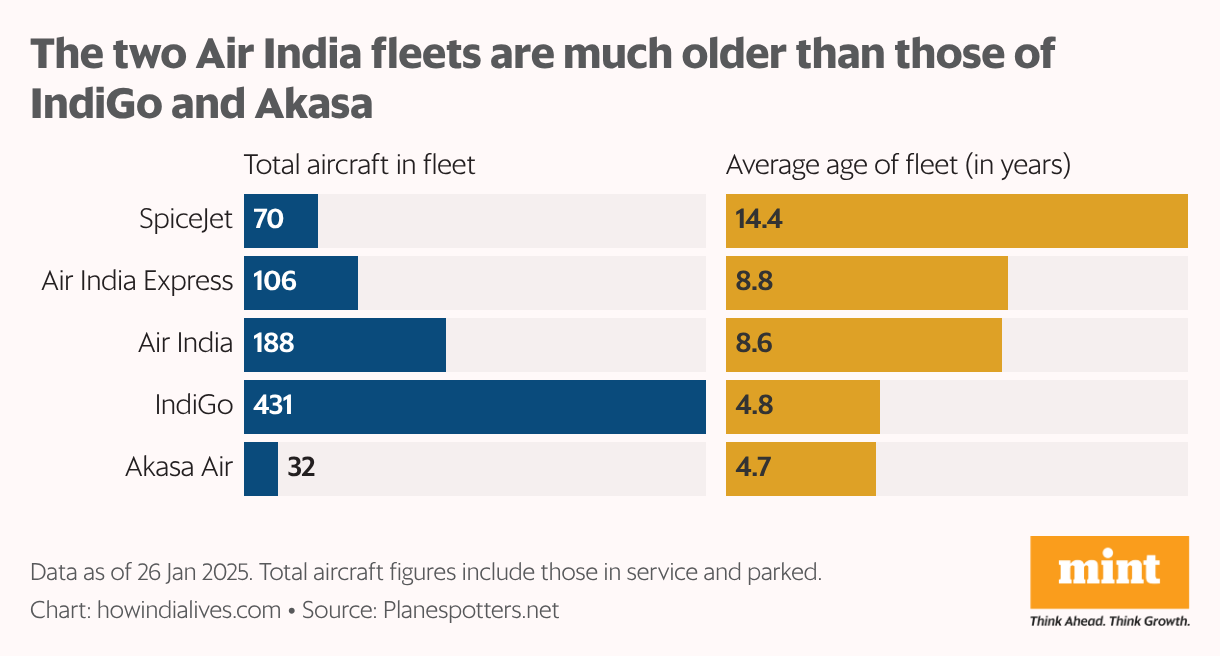

Both Air India and Air India Express need new aircraft to expand and gain passenger share as well as improve fleet capabilities. With a current average age of 8.6-8.8 years, their fleet is among the oldest among Indian airlines.

pilot seat

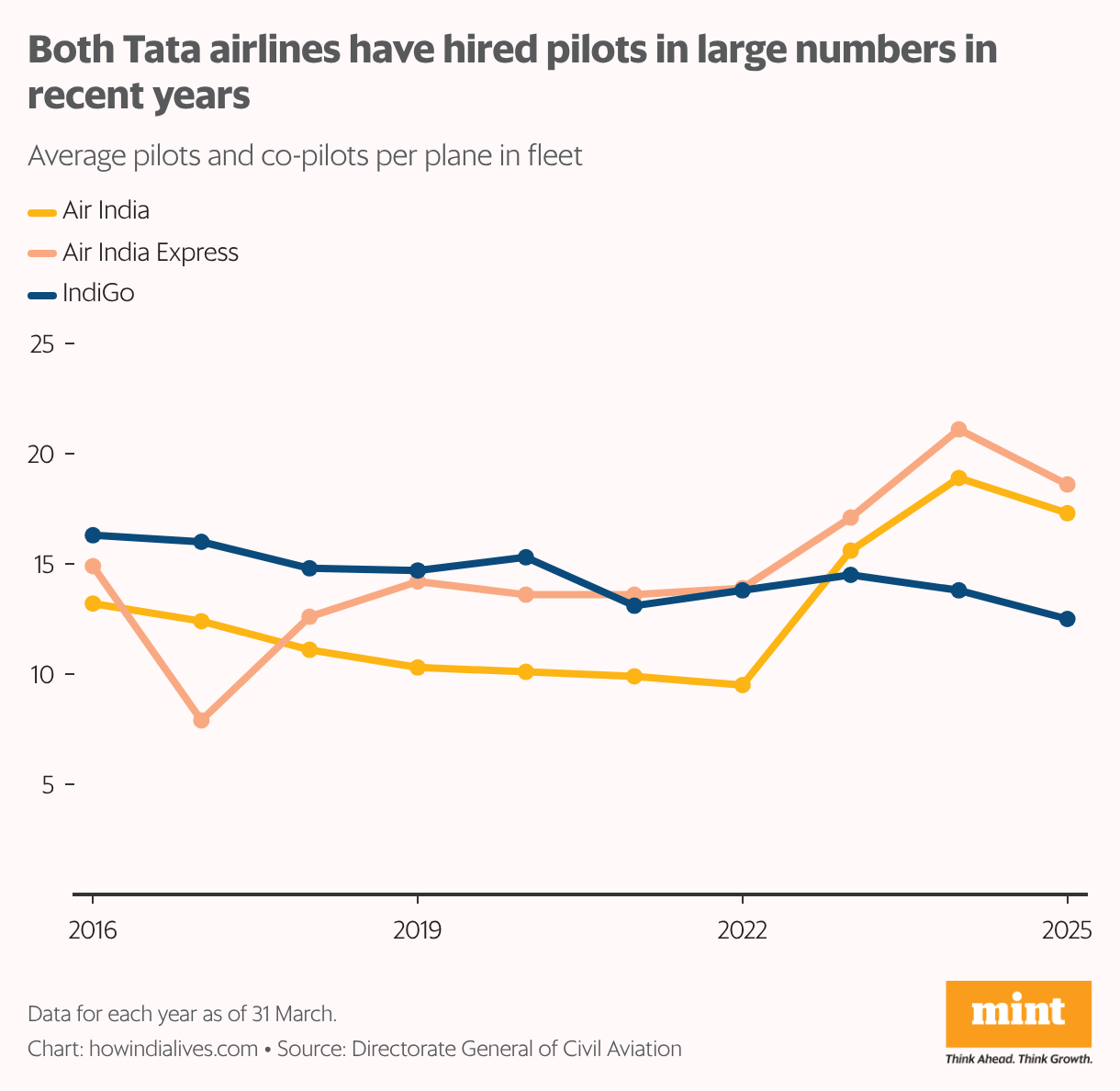

Another area where Air India needs to grow significantly is the strength of its pilots. Between March 2016 and March 2022, this number dropped from 1,411 to 1,116 for Air India. For Air India Express, the figure increased from 269 to 333.

Meanwhile, IndiGo rose from 1,747 to 3,791. But since then, both airlines from the Air India stable have hired aggressively and gained by absorbing other Tata airlines (Air India with Vistara and Air India Express with AirAsia) in late 2024.

Between March 2022 and March 2025, Air India’s pilot strength increased threefold and Air India Express’s increased sixfold. In total, as of March 2025, IndiGo was missing only 51 pilots. Although the need for wide-body aircraft was greater, which Air India operated more, they were outperforming IndiGo on an aircraft basis.

Pilot strength is also gaining importance in light of new regulations requiring all airlines to have more pilots than available.

loss of profit

Ultimately, all these steps, whether it is more planes or more pilots, need to be aligned to turn the business around, first at the operational level and then at the net level. Under the Tatas, Air India has shown good growth on the revenue side, whether inorganically (by acquiring other Tata airlines) or organically (by flying more passengers and generating higher revenues).

However, profitability remains elusive. In 2024-25, the two airlines posted a total net loss of approx. ₹9,700 crore. Disruptions such as collapse do not help the business, both reputationally and financially.

Last week Bloomberg reported that the airline expected a net loss of around 200 thousand ₹15,000 crore for 2025-26. Compare this with IndiGo, which reported similar net profit in 2023-24 and 2024-25.

The main cost for airlines is fuel, and crude oil prices are trending positively. Air India took advantage of this window, but not to the extent it had originally planned.

www.howindialives.com is a database and search engine for publicly available data.