India Inc’s two-speed revenue challenge in Q2

However, this recovery was offset by a precipitous collapse in non-core or “other” revenues; this contracted 1.5% year-on-year after five consecutive quarters of double-digit growth; This was the weakest figure in at least nine quarters since the second quarter of FY24. Sequentially, the decline was much steeper at 17%, reducing overall revenue growth to 2% from 5.5% in the previous quarter.

Experts say the weakening of non-core support could weigh on India Inc.’s headline revenue growth, which has supported higher non-core revenue throughout last year. “Headline revenue and net profit growth may remain muted in the second quarter and beyond (Q3) if non-fundamental weakness persists and core recovery remains shallow,” said Pranay Aggarwal, chief executive officer (CEO) of discount brokerage firm Stoxkart.

The sample is part of the entire listed universe of more than 4,000 companies.

lost income cushion

What explains this disappearing non-core revenue? Puneet Sharma, CEO and fund manager of Whitespace Alpha, calls this the beginning of “non-core normalisation”; This is a phase in which treasury earnings and one-time gains that increase revenues decline.

Other income refers to earnings earned outside of a company’s core activities, such as interest, dividends, or gains from asset sales.

Last year’s non-core base was inflated by one-off items such as asset sales, divestitures of subsidiary shares and treasury gains, which have now largely disappeared, Sharma said.

“With stock and bond markets stabilizing, mark-to-market gains have also narrowed,” Aggarwal said. “Meanwhile, weak commodity and forex trends lowered non-operating profits.”

In the absence of these gains, net profit growth fell to a four-quarter low of 7.5% year-on-year; Sequential profits fell 6.5%, continuing the 3% decline in the June quarter. Mint analysis.

Total profit after tax (PAT) for 551 companies ₹2.12 trillion.

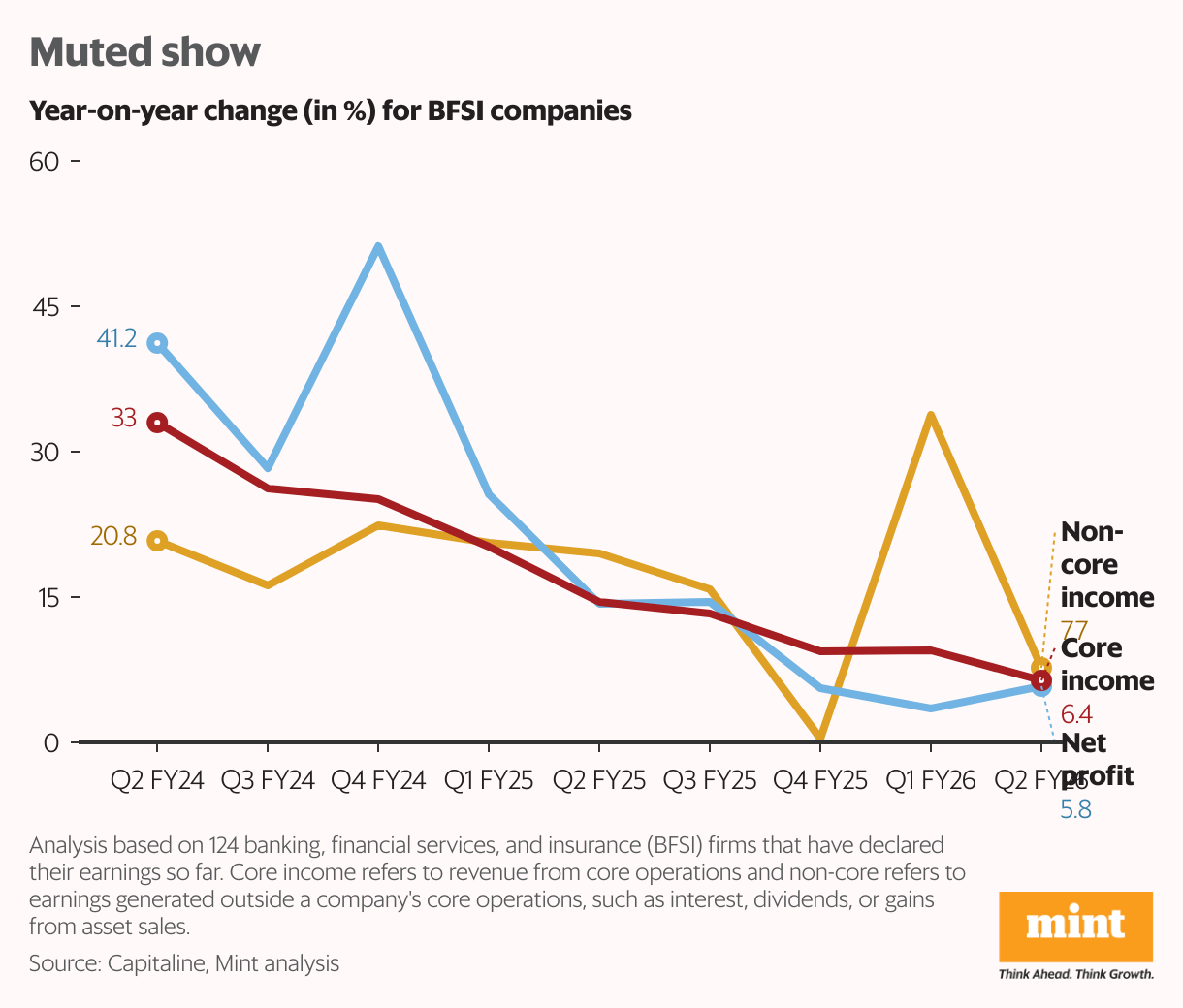

BFSI drag

The banking, financial services and insurance (BFSI) sector has challenged this “two-speed” model by weakening on both fronts.

a separate Mint Analysis of 124 BFSI firms in the sample found that both core and non-core revenues fell to their lowest levels in nine quarters, indicating stress in the operating and treasury areas.

According to Axis Securities, bank loan growth remained at 10% year-on-year as of September 19 due to a slowdown in retail and corporate loans. The brokerage expects banks’ core income to follow a gradual recovery in systemic credit growth but warned that rising bond yields could erode treasury earnings.

“Treasury revenue is likely to be quite low sequentially (in Q2), which will exacerbate banks’ profitability woes,” Axis Securities said.

It accounts for about 25% of BFSI. mint In the example, the sector dragged down India Inc.’s non-core revenues in the second quarter. The broader sample shows that India’s leading private banks generate 15-18% of their total revenue from non-core sources.

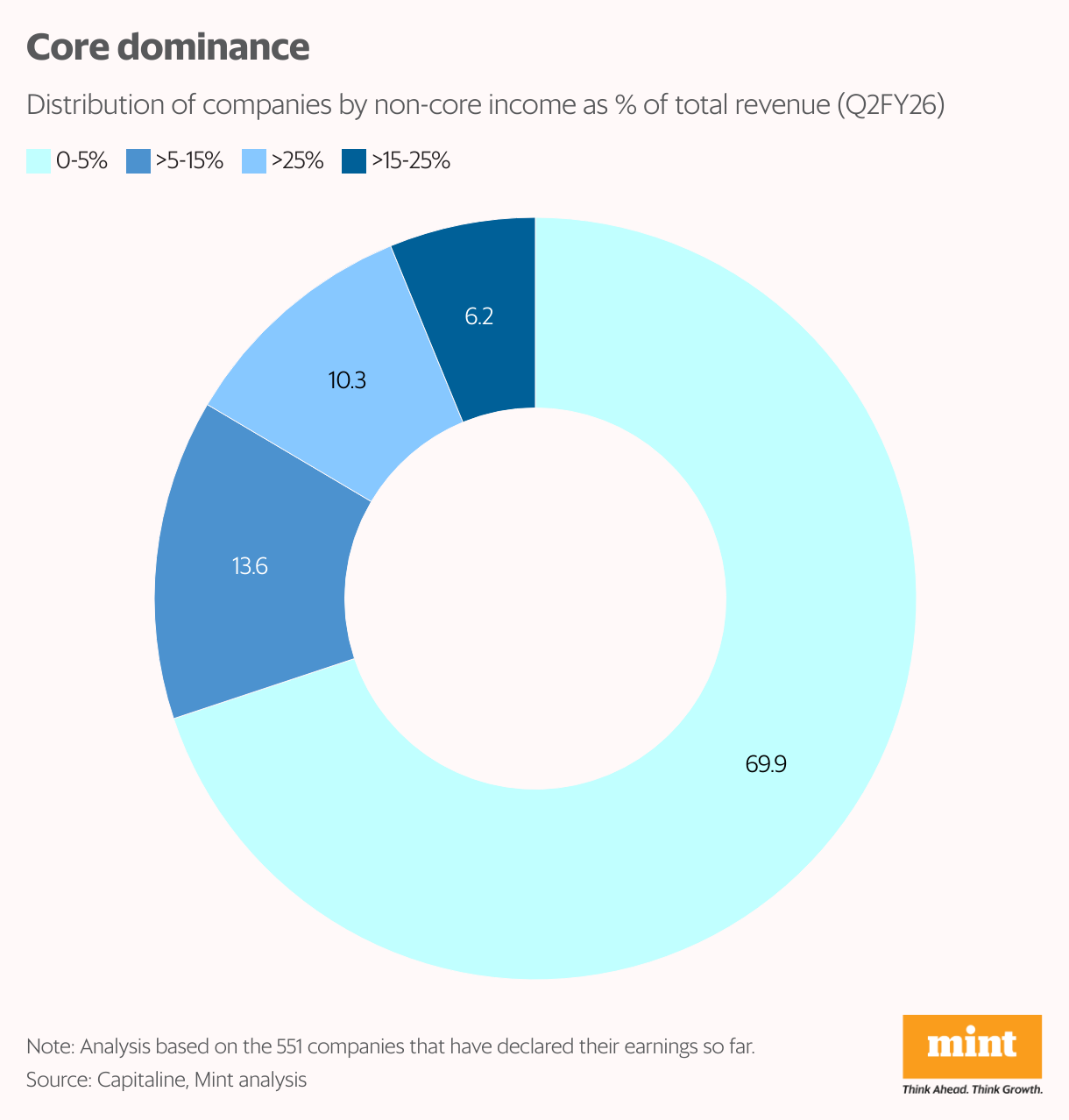

Income groups

The importance of other income is clear. About 10% of the sample earned more than a quarter of total revenues from non-core sources, which include banks, mining and real estate firms, where treasury profits, asset sales or mark-to-market gains have long led to large earnings swings.

Another 6 percent of companies generated 15-25 percent of their revenue through non-core means; this is a range that includes several leading private banks.

Roughly 14% of India Inc. is in the mid-band, generating 5-15% of total revenue from non-core sources. The data showed that this group includes various majors such as Reliance Industries, NTPC and Infosys, which periodically benefit from treasury or investment earnings.

The analysis found that the remaining 70% of firms generate 5% or less of total revenue from non-core sources.

Rising core income often signals stable consumption, increased corporate investment and real economic momentum. But does the contraction in non-core flows threaten the broader recovery?

Whitespace Alpha’s Sharma said that with the decline in non-core revenues, companies have lost an easy growth cushion and must now rely directly on core operations. “That’s a high bar to clear every quarter,” he said. “A mix of strong core performance and modest non-core support will be more sustainable.”

green shoots

It remains unclear whether the recovery in core income indicates a permanent demand revival or a temporary increase due to fiscal headwinds.

“It may be too early to call this a sustainable uptrend,” Stoxkart’s Aggarwal said.

Some of the recovery could be due to short-term fiscal support, front-loading government spending and festive season consumption rather than a broad-based recovery in private demand, he said.

At the same time, Aggarwal sees a visible recovery in various sectors, indicating a more sustained momentum.

“Chemicals and steel are benefiting from stable global prices and high capacity utilization,” he said. “Cement and real estate continue to gain from infrastructure momentum and resilient housing demand.”

IT services and pharmaceuticals are also contributing through stable export demand, healthy deal pipelines and tighter pricing discipline, he added. While Aggarwal expects IT, industrial sector and select manufacturing to offset some of the negative impact of weakening non-core revenues in the second quarter, he cautioned that this buffer may be limited.

“With midsize firms still struggling to grow revenues, much will depend on how broad-based the core recovery is,” he said. “Unless the core recovery extends beyond a few large firms, declining non-core revenues will continue to weigh on revenue growth.”

Reduced dependence on non-core resources also indicates a shift in corporate behavior. As operating strength returns, companies are shifting their focus from financial maneuvers to underlying revenue growth, Sharma said. He added that many firms are reallocating funds to capital expenditures and working capital as interest rates remain stable and excess cash yields lower returns.

“The slowdown in non-essential income is also a by-product of this healthy behaviour,” said Sharma. “This is a reminder that the true, long-term story of India Inc. will be defined by its core operations.”