Tamil Nadu’s new pension scheme broadly follows the guidelines of Old Pension Scheme

Pension under the Tamil Nadu Assured Pension Scheme will be based on 50% of the salary received in the last month of service; Under the Unified Pension Plan, it will be 50% of the average of the last 12 months’ basic salary. | Photo Credit: Getty Images/iStockphoto

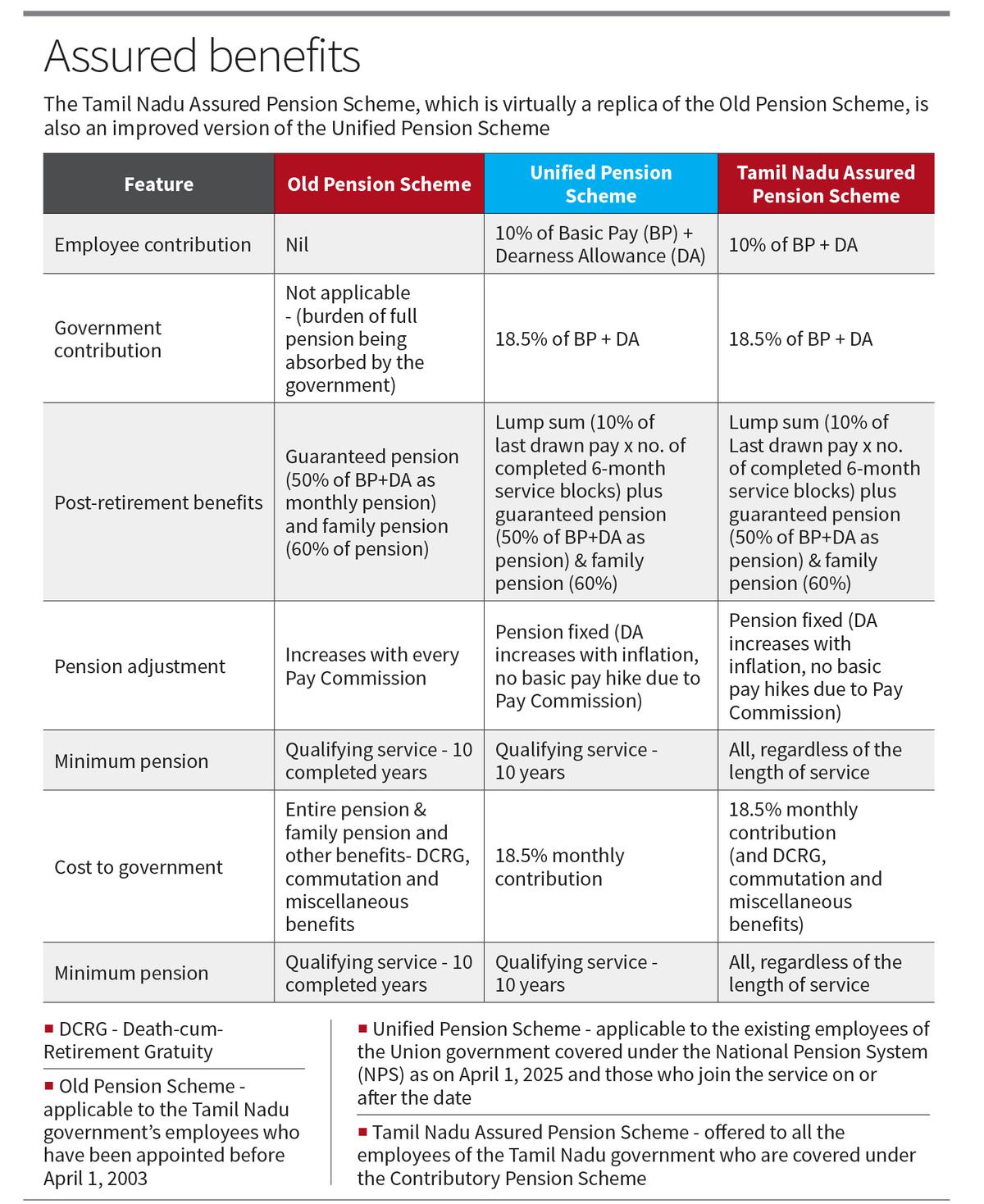

Almost a copy of the old Pension Scheme (OPS), Tamil Nadu Assured Pension Scheme (TAPS) is also an improved version of the Unified Pension Scheme (UPS).

Apart from the monthly individual contribution and pension revision at the time of formation of each salary commission, the proposed pension plan follows the general guidelines of the OPS. One of the key features of OPS is the death-retirement gratuity (DCRG).

For example, if those with a period of service of 20 years or more die in harness, gratuity not exceeding ₹ 25 lakh will be payable. This aspect is included in TAPS. As with OPS, the family pension will be equal to 60 percent of the pension. Inflation indexing will also be done.

Pension under TAPS will be calculated at 50% of the salary drawn in the last month of service, and under UPS will be calculated at 50% of the average of the last 12 months of basic salary.

If the retiree dies under UPS, only the legally married spouse will be eligible to receive the family payment, whereas in the case of TAPS, the family (i.e. the retiree’s nominated legal heirs) will be covered. While at UPS, there is minimum guaranteed pay if retirement is after 10 or more years of qualified service; Under TAPS, this payment will be given regardless of length of service.

Asked when the proposed scheme would come into force, a senior government official said legal formalities, including changes to pension rules, would need to be carried out first.

All existing employees under the Contributory Pension Scheme (CPS), amounting to around 6.24 lakh, are expected to switch to TAPS even if they are allowed to choose their retirement plans. The official observed that the government has decided to invest pension funds with Pension Fund Regulatory and Development Authority (PFRDA) instead of Life Insurance Corporation (LIC).

So far, the entire amount accrued under CPS, which covers those who joined government service on or after April 1, 2003, has been deposited in LIC’s Pension Fund. Till now, the State government was facing criticism from different quarters, including the Comptroller and Auditor General (CAG), for not using PFRDA for investment of funds on the grounds that such a move would yield higher returns. The CAG report on State finances for 2023-24, tabled in Parliament in October 2025, stated: “Previously the State had invested in DCPS [Defined Contributory Pension Scheme or CPS] Savings in both LIC and Treasury Bills earned lower interest than the General Provident Fund rate. This issue was highlighted in previous SFAR [State Finances Audit Report] reports. Currently, the Government deposits DCPS savings only in LIC and interest rates are in line with the General Provident Fund rate, currently pegged at 7.1%.”

‘viable model’

Another policy maker emphasizes that adequate precautions were taken when designing the new retirement plan. Projections have been made regarding the growth rate of State Own Tax Revenues (SOTR) for at least the next 15 years.

Although the value of the allowance increases each year, the rate of the pension obligation will be fixed at around 21% to 22% of SOTR.

According to the 2023-24 CAG report, the share of pensions and other retirement benefits was 22.5%; pensions stood at ₹37,696.81 crore and SOTR at ₹1,67,279 crore. Only a “conservative” growth rate of 8% was considered for SOTR.

“Therefore, we are quite confident that the retirement model we have developed will be feasible,” he added.

It was published – 04 January 2026 12:37 IST