Piramal Finance open to patient foreign capital, but no quick deals yet: CEO

“We have seen some good strategic investments taking place in the market recently; people are willing to invest in the Indian market for the long term; people see potential in business start-up, not just flip and sell,” Sridharan said.

Not just banks, India’s non-bank financiers have also received significant investments from overseas investors in recent times. The last of these was the decision of Abu Dhabi-based International Holding Company (IHC) to transfer $ 1 billion to Sammaan Capital.

Sridharan, who joined Piramal Enterprises in 2019 as managing director of its consumer finance business, was recently appointed head of the newly merged entity, Piramal Finance. The finance business was earlier called Piramal Capital & Housing Finance. It was renamed Piramal Finance in March 2025 and Piramal Enterprises merged with it in September 2025. As part of the merger, Piramal Enterprises was delisted from the stock exchanges on September 23. The merged Piramal Finance has received the approval of the Securities and Exchange Board of India and will start trading on November 7.

“We are a company that is 46% owned by the Piramal family, and the family’s perspective is obviously very, very long-term; it’s a cross-generational view of the business, and it’s rare to get that kind of patient capital,” Sridharan said.

He said the lender had little incentive to get investors involved and gave large shares to those with a limited view of the business. “This does not make sense to us and is not consistent with the company’s ethos,” he said.

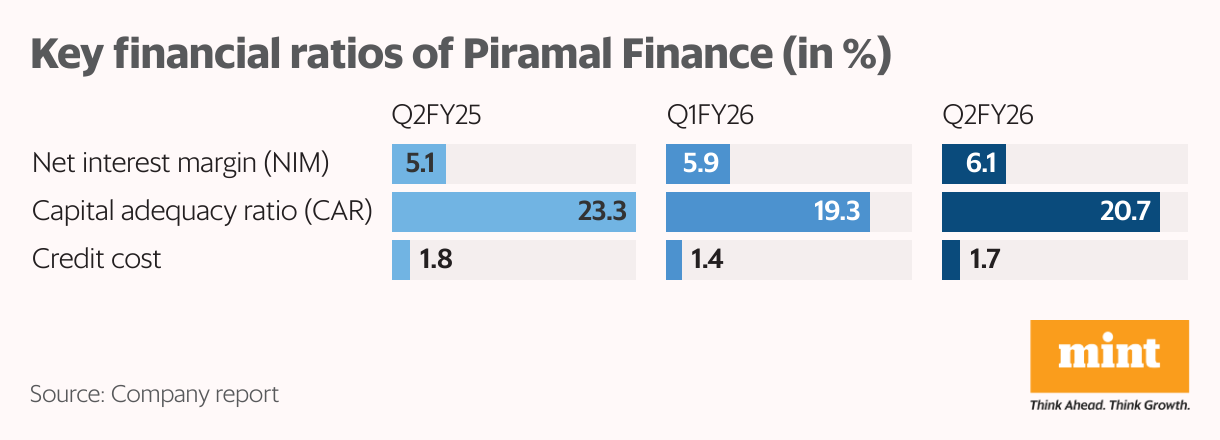

The lender’s capital adequacy ratio or risk buffer is 20.7%, well above the 15% regulatory requirement set by the Reserve Bank of India (RBI) for senior non-banking financial companies (NBFCs). RBI regulations classify NBFCs into four tiers based on their size, operations and perceived risk. In the upper layer, there are important names such as Tata Sons, LIC Housing Finance and Shriram Finance. Those in the top tier are subject to greater regulatory scrutiny than their smaller counterparts.

Given Piramal Finance’s plan to consistently grow its loan book by around 25% annually, the need for capital will arise sooner or later. Lender aims to double its assets under management (AUM) ₹1.5 trillion as of FY28. It had AUM at the end of the September quarter. ₹It aims to increase it to 91,447 crore. ₹1 trillion by the end of FY26.

“We are growing so much that we can burn through capital quite quickly and we need to be vigilant,” Sridharan said. “Our sense right now is that we probably won’t need capital through FY26. But we’ll probably need something at the end of that; we’ll see.”

According to Sridharan, the current growth of the business is also related to the markets the company caters to. Piramal’s financial services cater to semi-urban markets that are somewhat insulated from stress, he said.

“We are not a huge player in urban markets, major cities and metros. Both urban and rural environments have experienced some challenges in the last few months, but semi-urban India has done well,” he said.

The non-bank lender also plans to borrow up to $1 billion from the overseas market in the second half of the current financial year. “You can see us entering the international market again, and my expectation is that we should increase loans and bonds by at least $700-800 million, maybe even close to $1 billion if the environment looks good.”

Over the past few years, Piramal Finance has reduced its reliance on wholesale loans and moved into personal loans. Personal loans now make up 83% of the book.

“We have built a diversified retail business and now have over 5 million customers. ₹75,000 crore in retail AUM, making us one of the largest retail lenders in the country in the NBFC world,” he said.

Analysts appear pleased with the lender’s performance.

“The company has largely completed its transition to a retail-focused franchise with sharper underwriting, improved productivity and healthy risk-adjusted credit costs,” Motilal Oswal analysts wrote in an Oct. 17 note to clients. he said.

“With the balance sheet cleanup nearing completion and increased visibility of growth in core segments, we see compelling risk reward at current valuations.”

On wholesale lending, Sridharan said the lender will avoid high-cost and long-term loans or loans above that. ₹500 crore. Secondly, it will stay away from structured loan transactions and use ordinary loans. Third, it will avoid the risk of concentration when large loans are made to linked projects and companies.