Will interest rates rise after surge in oil prices over Iran-US war?

The conflict in the Middle East has continued into its second week and there are already major fears about the impact rising energy prices could have on people in the UK.

Rising prices and energy bills in particular could fuel higher inflation and cause the Bank of England to eventually raise interest rates.

Rising interest rates have knock-on effects elsewhere, including on people’s mortgages and savings.

Here, Independent It looks at how the war in the Middle East could affect rates and your finances.

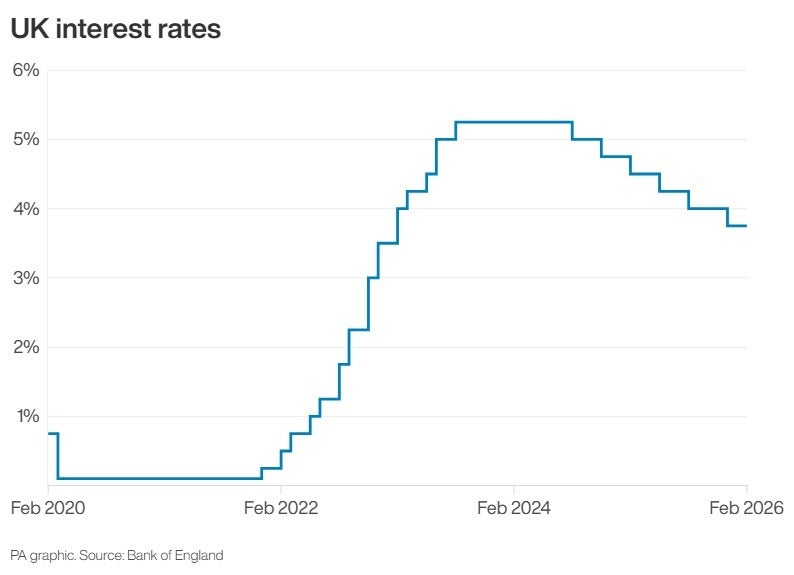

Will interest rates rise or fall?

Interest rates have been cut four times throughout 2025, with the Bank of England (BoE) cutting its main interest rate from 5.25 per cent to the current level of 3.75 per cent.

This was good news for mortgage holders renewing deals starting in 2023 or later and benefiting from cheaper borrowing costs, and it was expected that interest rates could fall further despite another possible rate cut at the BoE’s Monetary Policy Committee (MPC) meeting on March 19.

Some analysts were predicting three outages through 2026; This would bring us back to the 3 percent base rate last seen in December 2022.

However, these analysts quickly changed their minds in the last two weeks as geopolitical events threatened the global economy, rising inflation became a significant threat once again, and interest rates had the potential to rise in response.

Oxford Economics is predicting a postponement of the vote in March, but has raised its inflation forecasts for the second half of the year in line with rising energy bills, while noting that some MPC members are hoping for lower inflation to keep wage growth down – which this could clearly rule out.

UBS predicts the BoE will delay any potential cuts until April at the earliest, with most MPC members voting to go ahead with this one, effectively delaying their decision by a month for the picture to become clearer.

Get a free partial share of up to £100.

Capital is at risk.

Terms and conditions apply.

ADVERTISING

Get a free partial share of up to £100.

Capital is at risk.

Terms and conditions apply.

ADVERTISING

This is despite concerns about a weak labor market, which could lead two members, Swati Dhingra and Alan Taylor, to still vote for cuts, the bank’s research note said.

The prediction of being in a wait-and-see mode was echoed by RSM UK’s chief economist Thomas Pugh, who noted that markets – which change rapidly with world events rather than being a direct indicator of what will happen – are now more likely to indicate a future rise in interest rates rather than a cut.

‘Markets have virtually no chance of a nail-bited rate cut,’ Mr Pugh said Independent. “Even if they reach an agreement this week, I still don’t think you can cut interest rates, there is too much volatility right now.

“We’ve gone from pricing in two rate cuts this year to almost looking at one rate hike being priced in. This looks like the beginning of another cycle of inflationary shocks, hopefully not that bad, but still leaves a lot of uncertainty.”

“Normally the BoE can ignore one-off shocks because [inflation] cycle in one year. This was expected at the beginning of the Russian crisis, and it turned out to be a wrong policy. “With inflation having been above target for nearly five years and appearing unstable, they do not have the luxury of sitting back and reviewing the situation.”

Mortgages

Potential consequences of rising oil and gas prices include potentially higher food and goods costs, higher fuel prices, and an increase in mortgage deals through increased interest rates if the situation persists for a long time.

“Mortgage rates have fallen dramatically in 2025, helped by six rate cuts since August 2024, but the outlook today is very different from a week ago,” Bestinvest financial analyst Alice Haine said.

“Changing interest rate expectations are already being reflected in the market, with some major lenders announcing increases to their fixed-rate products in response to the crisis, and Moneyfacts data shows average two- and five-year fixed deals rose further last week.”

At the beginning of the week these were marginal adjustments; some contribute just 0.1 to 0.25 per cent on a set of deals – but recently this has increased both in the number of lenders pushing deals up and the amounts pushing them up. TSB increased deals by more than 0.6 percent, with two increases in one day.

.jpeg)

Mortgage deals in the market often change in response to swap rates, which are payment agreements between financial firms. When there is an expectation of future movement in the BoE’s base rate, swap rates may rise or fall in advance accordingly.

The UK’s housing market hasn’t been in great shape over the last 12 months but there have been signs of improvement recently; First-time buyer activity has increased due to falling mortgage rates.

Halifax’s house price index showed prices rose again in February this year, with the average property price up 0.3 per cent at just over £301,000.

Another rise in mortgage costs could threaten to derail the progress that is a key part of the growth of the UK economy.

Saving

The other side of the household finance equation related to mortgages is savings.

.jpeg)

When interest rates rise, people with money in the bank can often benefit because they can get a better return on their cash. For some time the best easy access rate on the market was 4.5 per cent at Chase, but already this week a sign or two has emerged that others, including some cash ISA providers, are increasing their rates to compete with this.

It’s not yet certain that the BoE will raise interest rates further, but a “pause” call in March looks increasingly likely; Another vote in April would offer a better chance to consider matters, perhaps a few weeks after the attacks in Iran began.

The approach of the ISA deadline of 5 April is a timely reminder for savers to both maximize the earning potential of their money and take advantage of tax-free allowances while they still can this year.