RBA rates rise not the sure thing that the commentariat cries

Conservative commentators who did not want a rate cut last year are calling on the RBA to raise rates tomorrow, but this may not happen. Michael Pascoe writes.

Bets in the money market are that Governor Michele Bullock will announce a 25-point interest rate increase on Tuesday afternoon. The herd follows comments favored by the national media, many of whom are unforgiving of the RBA’s rate cut last year.

This is against the odds in the market, but it is not impossible for the RBA to look beyond the headline figures and see that the case for a sudden increase is not clear, with both noise and irrelevant figures in the December quarter consumer price index. A quick and easy example: As Matt Grudnoff of the Australia Institute points out, almost all of December’s inflation was due to foreign travel and accommodation. explained.

It would be beyond foolish to think of rising unemployment in Australia because of hotel prices in London and Paris, or that such costs are contagious within the country.

The increase in the annual shortened average figure was only 0.05%, which was enough to stimulate the rounded headline. seasonally adjusted CPI For September, this rate was 0.2%. If you annualize it, it’s monetary Christmas all year round.

Why are some economists going against the flow on the RBA rate bet?

Politicized economists

Conservative columnists sometimes use a neat little slur against those who are not as hawkish on monetary terms as themselves: “pro-Labour economists”. They will no doubt be uncomfortable being called “LNP compliant”.

It might be more fair to call them “capital-adapted”, as their normal chorus is that labor is not cheap enough and productivity is not high enough because labor is not flexible enough, and “flexible” in this instance is often a euphemism for “cheap”. Labour’s dogma is that fiscal policy causes all inflation.

(No, Anika Wells’ expensive trip to New York was in the September quarter.)

What commentators strongly dislike is a “tight” labor market. What he never grapples with is the idea that we need something.

“Tight” labor market to encourage capital investment to increase productivity.

The RBA regularly wrings its metaphorical hands and ties itself in rhetorical knots about the labor market being “somewhat tight”, without defining whether it means “very tight”, and forever hoping that Goldilocks will be “just right” somewhere out there.

Unemployment dilemma

The biggest problem for the hawks is the idea that unemployment can be low and the labor market “somewhat tight” without causing runaway inflation, despite evidence in recent years that this is indeed possible.

You don’t have to be “Labour-aligned” to think the RBA would be wise to wait another month or three. Nonpartisan economist Gerard Minack said in his latest report for clients that he was not as confident as the market that the RBA would tighten this week, citing government subsidies affecting housing and utilities prices and “noise in the data” as the ABS was still trying to undercut its new monthly CPI series.

Minack notes that headline inflation is sticky, “partly because weak productivity implies current wage growth is too high and partly because high immigration is weighing on housing costs,” but he goes beyond pet shop galahs when looking at the RBA’s underlying assumptions, starting with the relationship between unemployment and wage growth.

“Wage growth for any given unemployment rate from 2013 was consistently lower than it had been in the previous 15 years,” he wrote. “If the post-2013 relationship continues, an unemployment rate of around 4% would lead to wage growth of around 3½%, a pace the RBA sees as consistent with its 2-3% inflation target.

“The second assumption is what level of wage growth is compatible with the Bank’s inflation target. In the past, the Bank seemed to believe that the sweet spot for wages was 3-3½% or 3¾%. Private sector wage growth is in this range (as measured by the Wage Price Index), but inflation is not within the Bank’s target range.”

Productivity galas

Yes, it’s a productivity issue; “a trend in unit labor costs rising too rapidly (three-year average) to be consistent with a return to the inflation target”.

The “famous macroeconomist” whom the AFR calls Minack hit the headlines in 2023. by saying ($) “Australian policymakers are ‘doubling down on a foolish strategy’ by relying on population growth rather than increased investment to grow the economy.”

He focuses on the issue of population or investment:

“Is government policy contributing to inflation? Every galah in the national financial press menagerie squawks about how much higher government spending is contributing to inflation. They got it wrong. The government policy contributing to high inflation is rapid population growth driven by immigration. Housing construction and rents are the two biggest items in the CPI. Both contributed to the inflation increase in the second half. Both are partly due to population growth.”

“Like the RBA, I was misled by the rebound in inflation by 2025. I should have given more weight to the effects of low productivity and rapid population growth on inflation. In hindsight, the RBA prematurely eased policy last year.

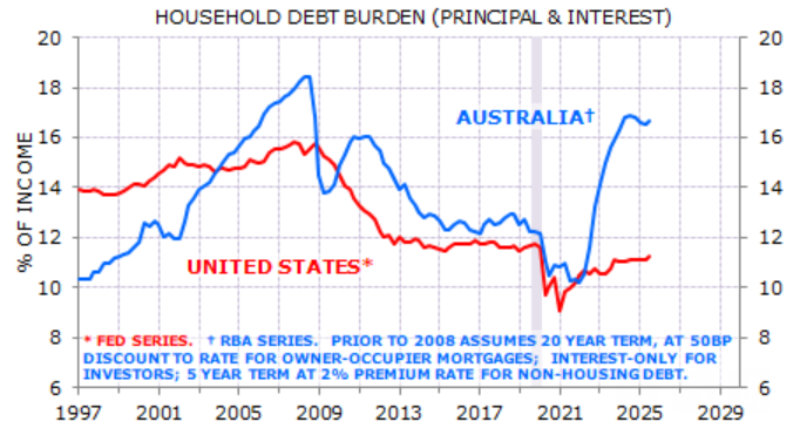

“But I still think policy is restrictive. For example, RBA tightening has had a much bigger impact on household finances than Fed tightening. If the Bank reverses course and tightens (in May, if not this week) it looks like Australia’s growth will start to slow in the second half.”

This last view is what Minack Advisors’ clients pay for. While the media focuses on how much mortgage lending can change month to month, the bigger call is that the Reserve Bank’s cut will lead to the Australian economy starting to slow down, which in turn has implications for investors.

And it’s not as if the economy isn’t growing strongly at the moment, remaining dependent on fiscal stimulus and two-pronged population growth to sustain consumption.

Considering downside risks,

The RBA’s still-new monetary policy board had better make sure it doesn’t jump into the noise,

From ABS or pet store.

Yes, some CPI numbers are up, but they could easily fall again this quarter. The rate hike assumption is already causing the RBA to do a backflip. If the numbers reverse again, it will be a more painful fiasco.

RBA explains what is needed to avoid rate hikes in 2026

Michael Pascoe is an independent journalist and commentator with five decades of experience in print, television and online journalism here and abroad. His book, Summertime of Our Dreams, was published by Ultimo Press.