Private health care. Why community ratings are failing the young

Younger members are abandoning private health insurance due to blurring of boundaries between insurers and providers and who pays for what and when. Claudia Weisenberger reports.

In a recent article, the CEO of Private Healthcare Australia, the peak body for the private health insurance industry, defended the use of ‘Community Ratings’, saying: “It reflects a fundamental principle: illness is not a financial choice and access to care should not depend on a person’s capacity to accumulate savings.”

The industry’s argument deserves fair scrutiny before addressing its contradictions.

Community rating requires insurers to charge uniform premiums regardless of health status. A 25-year-old pays the same rate as a 65-year-old with multiple chronic conditions. This cross-subsidization prevents people from being financially penalized for situations beyond their control.

Industry view. Why a health savings model could leave sick Australians behind

PHA’s objection to health savings accounts follows directly from this. Individual savings are a disadvantage for people who have chronic illnesses, congenital conditions, or whose employment has been interrupted, meaning they cannot save enough to cover their own expenses. This creates a two-tier system where wealth determines access.

These are serious arguments. Community rating protects people from being priced out for their health condition. However, when examining how the system actually works, contradictions emerge.

Choice or obligation?

Three days before defending the community rating, PHA proposed changing the Medicare Levy Surcharge from 50% to 140%; This has significantly increased the financial penalty for Australians who choose not to purchase private insurance.

If the community rating provides the claimed parity protection, the product must attract customers on merit. Not. One in seven Australians will drop insurance coverage in 2026. PHA’s response: Make leaving more expensive.

Markets that deliver real value rarely need coercion.

A pattern that requires increasing strain is held together not by value but by making alternatives worse.

Community rating only protects those who can afford the premium. And the pool is getting narrower. The share of hospital insurance for 25-49 year olds falls to 28% in 2024/25; a relative loss of 27% of individuals whose participation makes the community rating mathematically valid.

Insurance redistributes from the healthy to the sick.

However, under the current system, excess contributions do not constitute a transferable asset for the member’s later life needs. They fund the current care of others. A 30-year-old who has been paying premiums for 35 years contributes a significant amount, receives minimal compensation, and builds zero equity.

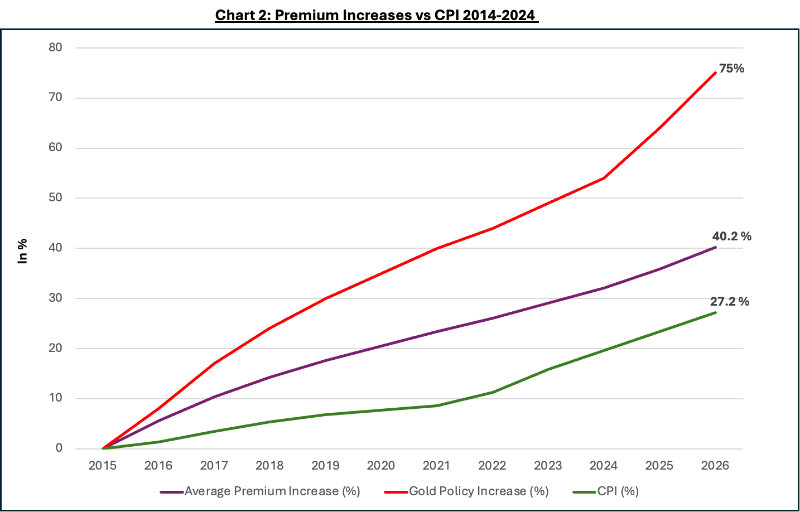

The affordability crisis exacerbates this. Gold policies have increased by 75% in the last decade, well above the 27% increase in inflation.

Proof of failure

Younger members face increasing costs for minimal claims while creating no assets for major health problems. Without a youth pool, community rating would fail arithmetically. The very migration that PHA aims to stop is evidence of failure.

PHA warns that health savings accounts will create a two-tier system where wealth determines care. still see APRAMore than half of Australians do not have private hospital insurance. They trust public hospitals

While waiting lists increased by 41.6%, premiums increased by 47%

According to Ministry of Health data, it has been for more than ten years.

There is now a two-tier system determined by wealth. Community rating protects those who can afford the premium. It does not protect those who do not protect.

Alternative models are available. By combining individual health savings with universal disaster coverage and clear safety nets, Singapore achieves superior health outcomes at lower costs. Cross-subsidization from young to old can be maintained without the need for increased coercion.

Private health insurance. Not fit for purpose and needs to be reset

Coercion is not solidarity

A system that requires tax penalties to be increased by up to 140 percent to maintain participation is not an exercise in solidarity. A model that fails to deliver value to the individuals who need it most.

When immigration meets repression rather than reform, when bonuses outpace inflation as younger members flee, when equality protections reach fewer Australians every year,

Structural failure is clearly visible.

Australians deserve better than mandatory premiums that fail to create equity and increase tax penalties when they choose otherwise. They deserve a system that works.

Health insurance premiums will cut more than hip pockets

This is the first in a series of private health insurance reforms. Next, we’ll examine where the $7.9 billion in taxpayer subsidies actually goes.

Claudia Weisenberger is a management consultant with deep experience in pharmaceutical, hospital transformations and strategic due diligence on four continents. It combines keen analysis with hands-on application.